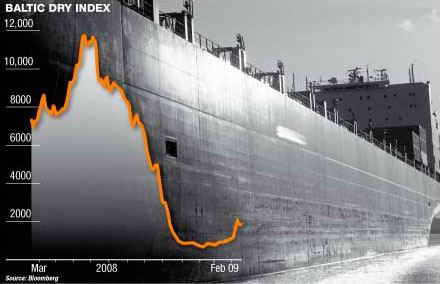

With the dry bulk market close to its lowest levels in months and indeed close to 2010 lows, ship owners could be heading towards scrapyards in a bid to relieve part of the market’s oversupply of vessels. Yesterday, the Baltic Dry Index lost further ground to end the session down by 1.91 percent to 1,795 points, weighed down once again by the ailing capesize segment, which lost an additional 2.5 percent.

With the dry bulk market close to its lowest levels in months and indeed close to 2010 lows, ship owners could be heading towards scrapyards in a bid to relieve part of the market’s oversupply of vessels. Yesterday, the Baltic Dry Index lost further ground to end the session down by 1.91 percent to 1,795 points, weighed down once again by the ailing capesize segment, which lost an additional 2.5 percent.As shipbroker Fearnley’s put it in its latest report, “Santa Claus didn’t come early this year”. Commenting on the Capesize market it mentioned that “whilst there has been anticipation in the market that bottom would soon be reached, rates continue to drop. For Australia to China, charterers are now targeting below USD 8 pmt, with last done at very low 8s. Tubarao/Qingdao is slowly approaching USD 20s, although there has been some resistance on this route. All in all the market needs a Christmas break, and hopefully activity will be speeding up early next year. However as it looks right now, expectations remain poor” said the report.

A similar situation is described for the panamax segment. “The Panamax market experienced limited activity and consequently continuous softening of rates in both hemispheres. The FFA´s traded steady arnd USD 16k for Q1, while 1 year TC period in the physical market was pending arnd USD 16-17k. Not many signs for market recovery last days of this year, especially Pacific has an oversupply of tonnage and lack of new orders to back up. Question now if market reached a level where owners and operators start picking tonnage again. Prompt Atlantic rounds fixed at USD 19-20k while the Pacific rounds sub 10k” it said.

As for the smaller ship segments (Handy/Supramax), Fearnley’s said that “not much fresh enquiry this week and quite dead in Bl.Sea/Med. Nevertheless large Supras are achieving USD 21/22k for TA rounds – 2/3 laden legs within the Atlantic which is actually not bad at all. As advised the pre-Xmas rush is keeping the market afloat but a large amount of tonnage is pouring into the Atlantic (ballasters from India etc.) and this should exerce downward pressure on rates by end Dec/1H Jan. USG is quite active on the petcoke side. Outlook: Flat. The FEast has been under real pressure over the past week. With the holiday season here owners are keen to just get vessels in employment with quick business then see the direction in the new year. Vessels are fixing for Indo rounds in the low 10´s and even hear of a large Supra fixing sub 10k opening N.China for a trip to India.

Nopac rounds are also few and far between but paying a tick more. Off WC India tonnage has been somewhat tight and the level seems to be around 15/16k for trips back to China with iron ore” Fearnley’s concluded.

It’s worth noting that a year ago, the BDI was standing at a hefty 3,258 points, up by more than 40% from today’s levels of below the 2,000 point mark. Still, activity in the demolition market is still on the low side, despite the fact that current rates offered by shipbreakers are at spectacular levels since the beginning of the year. Shipbrokers Golden Destiny said that “China is bidding aggressive rates by paying $450/ldt for dry/general cargo and India being close to break the barrier of $500/ldt for wet cargo. Bangladesh is still not fully reopened but a small movement has been recorded in last days with some vessels being beached in Chittagong, which seems promising for the future of the leader country in the shiprecycling industry. This week closed with 7 vessels reported to have been headed to the scrap yards equalling a total deadweight of 575,804 tons, indicating a 56% w-o-w decline. Tankers remain on the spotlight with positive demolition figures almost per week, whereas demolition activity in the container sector is standing at virtual standstill since the beginning of December. At a similar week in 2009, 16 vessels were reported for scrap equalling a total deadweight of around 343,305 tons while demolition countries were paying $300-$330/ldt for dry/general and $320-$340/ldt for wet cargo” said the report.