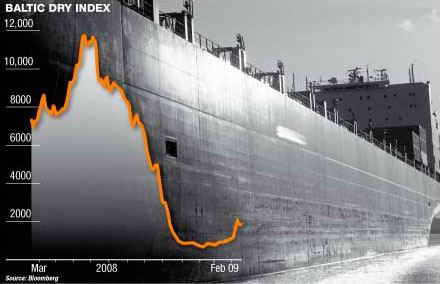

The dry bulk market isn’t exhibiting a “festive” behavior, thus cheering ship owners and investors alike. Instead, the industry’s benchmark has been falling this week, with the Baltic Dry Index (BDI) retreating yesterday to 1,886 points, close to its 2010 lowest.

The dry bulk market isn’t exhibiting a “festive” behavior, thus cheering ship owners and investors alike. Instead, the industry’s benchmark has been falling this week, with the Baltic Dry Index (BDI) retreating yesterday to 1,886 points, close to its 2010 lowest.

Both the capesize and the panamax segments were among the main losing sectors yesterday. During the course of the previous week, the Baltic Capesize Index managed to put a halt in its demise, by posting a marginal increase of 1% on a weekly basis. According to a weekly report from shipbroker Barry Rogliano Salles (BRS), the improvement was mainly due to a surge in demand from the big miners in the Pacific in the later part of the week. However the Capesize 4TC is now hovering around US$25,000 per day, the lowest point since the summer and well down on the average for the year. In India, Karnataka ore sellers will have to wait until mid January to hear a decision on their bid to overturn the state’s export ban. This week India’s top court gave the state additional time to respond to the miners’ legal petition. The Federation of Indian Mineral Industries has already estimated the ban will reduce India’s ore exports by 38% to 66m tons in 2010. The Karnataka High Court earlier upheld the provincial government’s decision to halt shipments overseas” said BRS.

It also warned though that based on trading in the futures market, rates are expected to continue their drift down in 2011, with 1H 2011 looking slightly more optimistic still than second half. Ship deliveries have slowed at the year end, but we can expect a resurgence in January with many owners postponing their December deliveries to the new year in order to have the more attractive ‘2011 built’ tag.

In a separate analysis, N.Cotzias Shipping Group mentioned that “we definitely get no short term trend patterns out of monitoring the indices, and that is for sure. If one expected to get a clear indication of the Dry bulk market just by studying the Baltic indicators we believe that this would never be sufficient, given the volatility and fluctuations that have become even more drastic during Nov & Dec of 2010. We expect this erratic behavior to continue well into 2011 with rather short term spikes to be followed by equal magnitude rapid falls. With more ships entering the market and with substantially lower increase in the demand for these, we feel that we should well embrace ourselves for falling ship prices, and many investment opportunities that will be there for the investors and owners that are seeking new fresh acquisitions. 2011 may well be a good year for the secondhand and resale S&P market and we will expect softer prices at more realistic levels to prevail” said the broker.

According to the report the past week’s interesting moves were the serious fall of the Panamaxes that have continued to contribute to the uncertainty with its weekly crazy looking ups and downs that have now started to fluctuate on a weekly trend. The stabilization of the Capes that show that there is the potential to make a rise, positive signs on the Cape market are seen by the secondhand sale and purchase and newbuilding front where some decent sized and decent priced capes changed hands or found a new “master” this week. Poly’s Hajioannou Safebulkers inked a Cape NB at Jinhai at $53mil backed by a 10y T/C at $25,000 per day. Also two NB resale capes were reported this week, with delay 11/2011 and 2/2012 by Noble who have agreed also on taking them in on long term T/C. FormosaBulk Energy 170k built 2002 was sold to undisclosed for 42.7mil while the smaller “Iron Brothers” 151k, 91 blt was sold to Chinese for $19.5mil said Cotzias.

As for China’s moves affecting the market, the weekly report on China from US-based Commodore Research & Consultancy said that Chinese commodity demand remains strong despite concerns over inflation. Thermal coal demand remains especially robust and coal shortages have become very severe in the central part of the nation. Steel output remains steady which has continued to result in firm demand for imported iron ore. Market sentiment has not yet fully recovered from inflation-related pressure however. Also, it mentioned that as a whole, coastal shipping rates to haul dry bulk commodities to ports along China’s coast have decreased moderately in recent weeks. Chinese commodity demand has remained strong but rates have come under pressure due to decreases in congestion. Congestion appears to be firming and rates to ship grain have begun to find support. Rates to ship grain from ports in Liaoning province (a major grain producing province in northeast China) to ports in Guangdong province (located in southern China) have increased to approximately $11.38/ton, $0.18 (2%) more than a week ago” concluded Commodore.