The Charter Market Gets Space To Breathe

The containership charter market has experienced improved earnings in 2015 so far. Charter owners have benefitted from supportive market fundamentals, reflecting a tightening of supply in the smaller section of the fleet where capacity has been shrinking. Further assistance has been provided by an apparent slowdown of a key aspect of the ‘cascade’ trend.

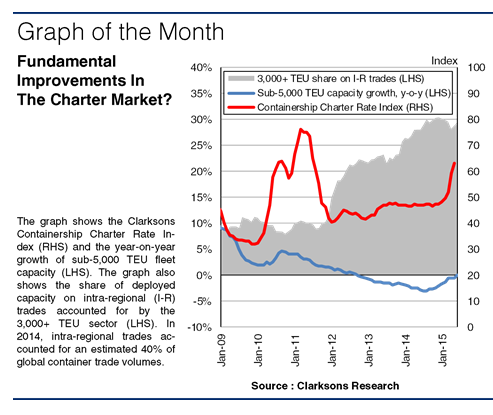

The Spring In 2015

Following a prolonged period stuck in the doldrums, containership charter market earnings have improved so far in 2015. Benchmark one year charter rates for a 4,400 TEU Panamax rose 51% 2015-06-23_upload_4107312_CIM1506between end 2014 and end May, between end 2014 and end May, reaching $15,350/day. Whilst Panamax rates began to pick up from mid-2014, improvements filtered down to the sub-Panamax sector in early 2015, with one year charter rates for a 2,750 TEU gearless sub-Panamax firming 66% between end 2014 and end May, to $13,250/day. During the same period, the Containership Charter Rate Index rose from 47 to 63 points.

Limited Supply

Improved charter market fundamentals have been evidenced by the limited level of idle capacity, which has remained under 2% of fleet capacity so far in 2015. By comparison, in early 2014 idling stood at around 4% of fleet capacity. As a result of both elevated scrapping and limited investment, supply in the sub-5,000 TEU fleet has been shrinking since late 2012, having contracted by 2% in both 2013 and 2014. When port congestion temporarily absorbed capacity in early 2015, this provided additional support to charter rates. But the crucial factor for the charter market has been an apparent slowdown of a key element of the ‘cascading’ trend. ‘Cascading’ in recent years has led to the re-deployment of larger ships (of 3,000+ TEU) onto the intra-regional trades where much of the charter owned fleet is deployed. This increased the availability of tonnage for operators to charter, and therefore put downward pressure on rates for charter market ships. Charter

Ships Get ‘Protection’

However, there has been a recent apparent slowdown of the ‘cascade’ of capacity onto these intra-regional trade routes. The proportion of deployed capacity on intra-regional trades accounted for by containerships of 3,000+ TEU increased rapidly from 10% at start 2011 to 30% by start December 2014 (see the Graph of the Month). However, this share has since flattened out at around 30%. This change in the ‘cascade’ trend has provided a degree of protection to the charter owned fleet by limiting growth in the supply of capacity available for operators to charter, thus supporting charter rates.

A More Solid Footing?

Whilst charter earnings have not yet reached historical averages, they are currently performing at their best levels for several years. These recent improvements reflect the alignment of key indicators in support of the charter market. The smaller section of the containership fleet is expected to continue shrinking, or grow at a negligible rate, in 2015 and 2016. Additionally, the market environment suggests that further cascading opportunities will remain difficult to find. This suggests that the supportive charter market balance which has developed could well be on a fairly solid footing.