(Part 1: Fundamental indicators)IntroductionLast week (August 5 to 9),

dry bulk shipping companies stood relatively flat. Some key developments that

moved share prices were Eagle Bulk Shipping Inc.’s (EGLE) and DryShips Inc.’s

(DryS) earnings calls, JP Morgan upping its target price on Diana Shipping Inc.

(DSX), China reporting the largest year-over-year production growth of 9.7%

since last December, and an unchanged consumer inflation rate compared to June’s

figure.Earnings summaryThe market took it as a negative that Eagle Bulk

Shipping Inc. (EGLE) either didn’t or couldn’t do much to increase the strength

of its balance sheet, which sent shares down the day after the earnings release.

While DryShips Inc. (DRYS) missed estimates, investors were quite pleased with

the several actions it took to increase its liquidity and financial

strength.China and industryAlthough data out of China was favorable, the

tapering of bond purchases in the United States (which economists widely expect

to begin in September now) has kept optimism in China at bay. As a result, dry

bulk shipping companies (with the exception of EGLE, DRYS and DSX) stood

relatively unchanged throughout the week. On the industry level, we’re also

seeing some changes in global trade, supply, ship prices, and shipping rates. In

this series, we’ll take a closer look at the following key dry bulk shipping

indicators.Dry bulk shipping weekly analysis (Part 2: Ship orders

fall)The importance of ship ordersOne measure that reflects managers’

expectation of future supply and demand differences is the number of ships on

order. When managers expect future supply to increase more than demand, they

refrain from purchasing new ships. However, when they expect demand to outpace

supply growth, companies return to the shipyard to place new orders, on the

condition that they expect to generate profits with the new vessels. So rising

ship orders often indicate that shipping rates will rise. Since dry bulk ships

usually take one to two years to construct, the indicator is often more relevant

to long-term investment horizons.Ships on order experience sharp fallOn

August 9, the number of dry bulk ships on order as a percentage of the existing

number of ships fell sharply from 10.24% a week ago to 10.03%. The dry bulk

orderbook as a percentage of existing capacity (measured in deadweight tonnage,

DWT—the weight ships can safely carry on the water—and also including the ships

under construction) fell to 17.43% from 17.64% a week ago.This may look

negative, because it means managers placed fewer new orders compared to the

amount of ships entering construction or supply. On the one hand, a sharp

decline in ship orders could mean managers were expecting or are expecting

shipping rates to recover in the future and that we’re getting closer to those

dates. On the other hand, if managers are wrong, it could mean larger supply

growth over demand growth, which will hurt shipping rates.Long-term trend

and implicationNonetheless, the rebound we’ve seen in new orders since the

beginning of the year is still a positive sign that managers see much of the

large backlog has cleared, the worst is over, and the supply-to-demand balance

will normalize. This will translate into higher margins, earnings, and share

prices for dry bulk shipping companies such as DryShips Inc. (DRYS), Diana

Shipping Inc. (DSX), Knightsbridge Tankers Ltd. (VLCCF), Safe Bulkers Inc. (SB),

and Navios Maritime Partners LP (NMM). Short- to medium-term fundamentals

may still differ for each company. This is because dry bulk vessels can take up

to two years to construct and firms such as Safe Bulkers Inc. (SB) and Navios

Maritime Partners LP (NMM) are subject to lower revenue when some of their

valuable contracts mature. But the pace at which managers have been placing new

orders (unlike tankers) suggests companies are rather optimistic regarding the

dry bulk shipping industry’s outlook—likely due to large supply and demand

growth differences in the near future. Moreover, since the value of a company is

based on future expected earnings potential, the market has started to price in

the favorable long-term outlook. If shares do fall, they’ll likely find

bidders.Dry bulk shipping weekly analysis (Part 3: Construction

rises)Ship construction activityPart 2 of this series explains how ship

orders can illustrate managers’ expectations for future supply and demand

differentials. But new ship orders don’t always translate into new constructions

right away. Sometimes, shipping firms specify a particular date of delivery for

the new orders. If the delivery date is farther out, ship construction firms

will delay work. So construction activity, on top of ship orders, gives

investors further insight into managers’ expectation of future supply and demand

differences as well as when and by how much supply will grow in the

future.

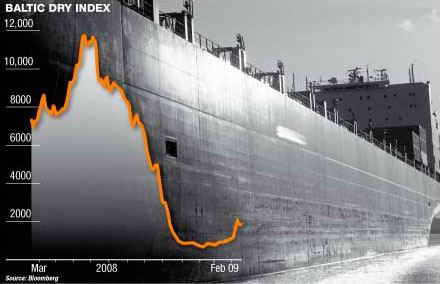

Could construction activity be showing some signs of recovery?On August 9, the number of ships under construction as a percentage of existing vessels reversed a four-week decline, increasing from the prior week’s 4.26% to 4.34%. It’s too early to tell whether construction activity will continue to rise, but it’s a positive sign that higher shipping rates are nearer in sight—especially combined with the sharp declines in ship orders we saw in Part 2.Construction activity started rising in 2009, as shipbuilding firms began work on a large number of orders, which coincided with a peak in the number of ships ordered at ~50%. Activity has fallen since, because managers placed fewer orders post-2009, when they saw how much they’d over-ordered. Orders have continued to slip as ship construction firms worked through the large amount of ship orders. While managers have returned to the shipyard to place new orders, they haven’t needed the new ships immediately. As we’ve said in previous updates, the weakness in construction activity shows that managers are in no rush to receive these new orders and expect shipping rates as well as profitability to remain low for at least the short term. But last week’s data may just be the beginning of higher construction activity in the foreseeable future.Inference and outlookInvestors will be concerned that such an increase in construction activity may increase supply more than wanted in the future, which is why low construction activity could still have been positive for shipping companies. While that’s something to look out for (which stresses the importance for investors to look at several key indicators instead of just one) there’s a window of up to two years for that to occur, because of how long it takes to build a dry bulk ship.At the moment, we could take the recent data as neutral for dry bulk shipping companies such as DryShips Inc. (DRYS), Diana Shipping Inc. (DSX), Knightsbridge Tankers Ltd. (VLCCF), Eagle Bulk Shipping Inc. (EGLE), and Safe Bulkers Inc. (SB). As long as shipping rates continue to turn around, you may see higher construction activity as a positive. But if construction activity continues to rise without improvements in shipping rates, it will be negative.Dry bulk shipping weekly analysis (Part 4: Capacity growth)Why is capacity important?Although ship orders and construction activity are useful to get the insiders’ perspective, investors must also look at capacity growth to see whether it meets demand so that they don’t rely totally on managers, who can get caught up in the day-to-day operation without seeing the bigger picture. When capacity grows faster than demand, competition rises among individual shipping firms as they try to use idle ships and cover fixed costs. This lowers day rates, which negatively affects bottom line earnings, free cash flows, and share prices for companies. But when demand grows at a faster rate, it’s positive for dry bulk shippers.Annual capacity growth falls to a new lowOn August 2, dry bulk capacity, measured in deadweight tonnage (DWT, the weight a ship can safely carry across the ocean) and published weekly by IHS Global Limited, rose to 608.78 million DWT, while annual growth fell to a new low of 5.70%. Year-over-year growth using the last four weeks of data, which smooths out short-term noise, fell from 5.91% during the prior week to 5.83% this week.Driven by large placements of new ship orders, shipping capacity had a huge run over the past two years, as companies expected global trade growth to continue at a record. The recent decline in year-over-year capacity growth is a positive development because total dry bulk demand grew by just 5.1% during the first five months of 2013, as reported by RS-Platou, an international ship and offshore investment bank. Further growth in iron ore shipments coming out of Brazil and Australia due to capacity expansions (which we’ll discuss in later parts of this week’s update) as well as an expectation of a record grain output in the United States should lift demand higher towards the end of the year.Real test to come later this yearBut the real test will come later this year. Last year, several dry bulk shipping companies pushed back deliveries as China’s economic growth fell and shipping rates fell to a record low. The eight-week average weekly growth rate, shown in the chart above, fell to an average of 0.075%. Since the start of this year, capacity has grown ~4.08%. Unless we see the average weekly growth rate come down below 0.10%, capacity will likely grow by 7% this year, which could limit further upsides for dry bulk stocks such as Diana Shipping Inc. (DSX), Eagle Bulk Shipping Inc. (EGLE), Knigthsbridge Tankers Ltd. (VLCCF), Navios Maritime Partners LP (NMM), and DryShips Inc. (DRYS) until the end of this year. This could also harm medium-term share prices—especially if several maturing shipping contracts were drafted out above current market rates. Nonetheless, the current trend is positive for the industry’s long-term outlook. If investors stay focused on the favorable long-term prospects, dry bulk shipping companies will find support.Dry bulk shipping weekly analysis (Part 5: Electricity output)The significance of China’s industrial outputChina’s industrial output—crude steel and electricity outputs, to be specific—are bellwethers of demand for raw material shipments. When industrial production rises quickly, so does demand for raw materials like iron ore and coal, which often accompanies higher domestic production and imports. Since dry bulk ships take one to two years to construct, supply is quite inelastic. So changes in imports have large impacts on shipping rates, and vice versa.Industrial output rises highThe year-over-year change in China’s industrial output rose to 9.4% in July from 8.9% in June. Industrial output has fallen from last year’s December high of above 10% growth, when the government clamped down on soaring housing prices and shifted its stance towards lower economic growth in return for a more sustainable growth rate. But since second quarter GDP growth came in at exactly 7.5, the target the government set for the year, there’s an incentive for the government to increase public stimulus. This is likely what drove industrial output higher.Electricity output rises to a highFor the same month, electricity output rose to a high of 10.2% year-over-year growth—higher than June’s 8.1%% and a record since September 2011. Although electricity output doesn’t directly reflect crude steel production, it still depends on industrial activity that uses a lot of crude steel in constructing buildings and manufacturing cars. While the July update for crude output isn’t available, in China, most steel manufacturers are affiliated with the government. This means they have a responsibility to keep workers employed, or social unrest due to unemployment can create trouble. Plus, unless they’re losing significant money, companies have noted it’s often better to keep output constant rather than shut furnaces down only to restart them later. So it would be surprising if crude steel output falls substantially when we update it.Bulls and bearsInvestors have worried since a few months ago about whether the government’s move to cool the property market down would hurt industrial output. While the bulls will say industrial output continues to grow positively and hasn’t fallen off a cliff, the bears will point out that output growth isn’t as high as it was before. They’re both right. Compared to before the financial crisis, in 2010 and 2011, industrial output consistently stayed above 10% for steel and electricity output. This time around, though, growth reports have been lower, as the government’s not so eager to energize the economy by pumping more stimulus into it like it did before. This is because China’s transitioning to a consumption- and private enterprise–led economy. Just like how a job switch can be time-consuming and take some ramp-up time, the switch will take a while.Implication for shippingBecause share prices reflect the future outlook of a company’s earnings potential, lower output growth has negatively impacted share prices of shipping companies like DryShips Inc. (DRYS), Diana Shipping Inc. (DSX), Eagle Bulk Shipping Inc. (EGLE), Safe Bulkers Inc. (SB), and Navios Maritime Partners LP (NMM) in the short term. While China’s economic growth is unlikely to expand as fast as it once did, the market is starting to realize this, knowing that the world isn’t going to collapse. This will be positive for long-term share price movements driven more by long-term fundamentals.Dry bulk shipping weekly analysis (Part 6: Producer inflation)The significance of inflationAnalysts keep an eye on China’s inflation numbers because they show what policymakers may (or will) do with the country’s monetary policies. 1 When inflation rates are high, policymakers will tighten monetary policies to lower spending in the economy, which often slows down manufacturing activity. As China’s manufacturing activity is a key driver for dry bulk and oil trade, lower economic growth means lower revenues and earnings for shipping companies.Producer prices tick up in JulyConsumer price index (CPI) grew 2.7% in July—unchanged from June’s data. On the other hand, the year-over-year change in producer price index (PPI) rose to -2.3%—higher than June’s -2.7%. The consumer price index reflects the price of goods that consumers in China spend on average, whereas the producer price index reflects the wholesale prices received by domestic producers of goods and services.

Analysts widely consider the two indexes because a high inflation rate (although often suggesting strong demand and economic growth) will lower the purchasing power of money and lead to hyperinflation (extremely high inflation that’s gone out of control). This can lead to an economic collapse down the road, because either goods will become too expensive to purchase or money will become worthless. When money is worthless, the financial system collapses.Positive conclusion from low inflationJuly’s tame growth in the CPI was positive for monetary policy, while an uptick in PPI growth shows demand isn’t collapsing like it did in 2011. Because PPI is already near a cyclical low, if there’s a financial problem, the central bank can intervene to hold the economy from falling off the cliff. While cheap credit is definitely history, as China reins in on shadow banking activity—which Diana Shipping Inc. (DSX)’s CEO recently said in its second quarter earnings call—the probability that issues within China’s financial sector will spillover to other parts of the economy is quite limited.

This bodes positive for dry bulk shipping companies such as DryShips Inc. (DRYS), Diana Shipping Inc. (DSX), Navios Maritime Partners LP (NMM), Safe Bulkers Inc. (SB), and Knightsbridge Tankers Ltd. (VLCCF). A crash like the one we saw in 2008 is unlikely to happen.Learn more about indicators that drive the dry bulk industryContinue to Part 7: Australia’s exports or go back to Part 1 to see the list of indicators.1. Monetary policies are tools that central banks use to increase or decrease demand for loans through changes in the base interest rate or the bank’s ability to lend out money.Dry bulk shipping weekly analysis (Part 7: Australia’s exports)Australia: The commodity giantAustralia, one of the world’s most natural resource–rich countries, has become one of the largest commodity giants over the past decade, on the back of China’s golden age investment-led economic growth of 10% each year. Accounting for close to 50% of total iron ore shipments to China—as well as a percentage of total iron ore seaborne export—Australia’s iron ore export volume is a key indicator of dry bulk shipping demand. When Australia’s iron ore export volume grows at a rapid pace, it means more business for shipping companies, which bids up shipping rates. On the other hand, if export volume stagnates or falls, it will negatively affect shipping rates.Australia pushes ahead with larger exportAlthough the market has fallen due to China’s tolerance for lower economic growth since the start of the year and experts widely agree that China’s economy will never grow as fast as it did before the financial crisis, Australian iron ore producers haven’t slowed their production and shipments. Instead, they just exported a large amount (36.5 million metric tonnes) of iron ore in June—close to the record amount of 37 million metric tonnes of iron ore in May. The average iron ore import (using the last six months of data) rose from 33.4 million in May to 33.5 million in June. On a year-over-year basis, export rose by 30% (see the chart below).Capacity addition to support export volumesAnalysts predict export from Australia to increase further, as they expect the country to add approximately 100 million metric tonnes of capacity this year—half of which Rio Tinto will supply. That’s an extra 8 million per month. During the last quarter of 2013, Australia exported an average of ~45 million tonnes of iron ore per month. A maximum increase of 8 million tonnes of iron ore monthly should add roughly 17% annual growth to Australian iron ore exports towards the end of this year. In Diana Shipping Inc. (DSX)’s latest earnings call, it announced that it expects iron ore trade to increase by 10% in 2013.Since Australia’s iron ore export makes up ~13.5% of the world’s total dry bulk shipments, a 17% increase will add ~2.3% to global dry bulk shipping trade volume. This will have a positive impact on shipping rates—Capesize vessels in particular—which dry bulk shipping companies such as DryShips Inc. (DRYS), Diana Shipping Inc. (DSX), Knightsbridge Tankers Ltd. (VLCCF), Navios Maritime Partners LP (NMM), and Safe Bulkers Inc. (SB) will benefit from.Dry bulk shipping weekly analysis (Part 8: Shipping rates)Supply and demand drives dry bulk shipping companiesUnlike imports data that aren’t widely available on a weekly basis, shipping rates (which reflect the difference in supply and demand), are collected on a daily basis at the London-based Baltic Exchange and published as the Baltic Dry Indexes (BDI). These indexes reflect the daily shipping rates to transport key dry bulk raw materials in the spot market. When demand outpaces supply growth, shipping rates tend to rise. But when an increase in supply doesn’t meet with demand, shipping rates fall. 1 Lower rates in an uptrend Last week, the Baltic Dry Index fell from 1,065 on August 2 to 1,001 on August 9, dragged down by declines in Capesize and Panamax vessels. Excess supply growth in Panamax vessels continues to put downward pressure on rates. But current levels still stand higher than what they were for the most part of 2013. Shipping rates in the spot market have risen lately due to the lower capacity growth we saw in Part 4, the higher oil prices that shipping companies are passing on to customers, and increased iron ore trade from Australia (see Part 6) and Brazil.Higher imports have been driven by continuous growth in China’s steel output, a record-low inventory figure of ~57 million tons in March (a number unseen for three years), and a decline of ~$40 per metric tonne (28%) since the government began tightening the property market in February that has made imported iron ore more attractive. Capesize vessels, which primarily haul major bulk materials such as iron ore and coal, have benefited most.Future developmentBut as imported iron ore prices have risen to a recent high of $135.5 per metric tonne, the likelihood of lower iron ore imports has or will negatively impact rates in the near term. Nonetheless, investors expect iron ore prices to remain low as Australia and Brazil boost capacity, as we discussed in Part 6, by the end of this year, which would be positive for dry bulk shippers. Low inventories and continuous steel production China—despite what markets have feared—should help absorb the increase in supply. Plus, as U.S. rain improves prospects for a record corn output this year, analysts expect grain shipments to grow by 8% annually, likely to support Panamax rates.(Read more: Why the Baltic Dry Index has decoupled from the Chinese market)Shipping rates outlookIf the capacity trend we’ve seen in Part 4 continues to show improvements, we’ll likely end up seeing higher shipping rates in the second half of 2013 compared to the first half—a positive for companies such as Diana Shipping Inc. (DSX), Navios Maritime Partners LP (NMM), DryShips Inc. (DRYS), Knightsbridge Tankers Ltd. (VLCCF), and Safe Bulkers Inc. (SB).Learn more about the key performance indicators of the dry bulk shipping industryContinue to Part 9: Forward contracts, or go back to Part 1 to see the list of indicators.1. The two main revenue generation models in the shipping industry are spot (voyage) and time (period) charters. “Spot charters” refer to the one-time price of shipping a specific amount of raw material, while “time charters” reflect the price of borrowing a ship’s service for a specific period. “Time Charter Equivalent” (TCE), which converts spot charters (specified in $ per ton) to time charter rates ($ per day), is often used to compare companies in different markets. The two often mirror each other over the medium and long terms. Dry bulk shipping weekly analysis (Part 9: Forward rates) What are forward contracts?If there are shipping rates for today, then there’s also the expectation of tomorrow’s rates. Companies use forward contracts to lock in the availability of resources in the future at a set price. The dry bulk shipping industry—which transports key dry bulk materials such as iron ore, coal, and grain—is no exception to this practice. When shipping companies negotiate the rates of shipping raw materials, they consider future expected supply and demand. If the rate of renting a ship and service in a forward contract is higher than the current rate, it’s often a positive indication that shipping rates will rise. Higher shipping rates mean higher revenues, earnings, and free cash flows—and vice versa.Higher forward contract pricesAfter we saw forward contract charter rates for Capesize vessels (ships that mainly haul iron ore and coal) increase throughout the past few weeks, with the spread between the three tightening, all three contract rates (current quarter, forward one-year, and forward two-year) have pulled back on a weekly basis.Rates have all drifted lower over the past few years because shipbuilders delivered more than a necessary amount of newbuilds (new ships), driven by companies’ over-optimism toward future profitability. But since last year, shipping rates have started to base because several companies began to report negative earnings, capacity growth improved because of lower new ship deliveries, shipping companies continue to scrap older vessels, and shipment growth continues in dry bulk iron ore shipments.Unlike before 2010, when people in the industry expected new deliveries to continue to hurt future profitability, contracts that are farther into the future have priced above nearer-term rates for the past two years. This is happening because people in the industry expect supply growth to fall even farther in 2014 and 2015, as companies plan to allow the current excess capacity condition to alleviate and profitability to improve.Current rates rise above future ratesMore importantly, the current quarter’s time charter rates have now moved above rates for contracts that are farther into the future—something we’ve spoken of in prior articles. This reflects an unexpected increase in short-term demand. While this happened a few times in late 2011 and 2012, increases in one-year and two-year forward contracts didn’t exactly materialize back then. While we saw a decline in all three contracts, if we continue to see positive upward movement in forward one- and two-year rates, Capesize vessels should see a real recovery towards this end of this year.

With additional iron ore capacity coming out of Australia and Brazil, and China’s industrial output remaining positive, we could see positive surprises toward the end of this year in the dry bulk shipping industry. This bodes well for the long-term outlook of dry bulk shipping companies such as DryShips Inc. (DRYS), Diana Shipping Inc. (DSX), Safe Bulkers Inc. (SB), Navios Maritime Partners Inc. (NMM), and Knightsbridge Tankers Ltd (VLCCF), and the market will likely begin pricing them in over the next few months.Dry bulk shipping weekly analysis (Part 10: Ship prices) Why should you watch ship purchase prices?Purchase prices for ships are often good indicators of financial health in the shipping industry. When shipping demand grows more than the supply of ships, shipping companies place additional orders, which drives up purchase prices. Plus, when firms are able to charge higher prices for transporting goods across the ocean, profitability rises, and so does the value of ships.Panamax stabilizing, Handymax/Supramax risingDuring June, the average vessel prices for 15-year-old Panamax, Handymax/Supramax, and Handysize ships rose to a nine-month high.• Panamax: $9.5 million to $10.0 million (5.3% increase since May)

• Handymax/Supramax: $9.5 million to $10.0 million (5.3% increase since May)

• Handysize: $13.5 million to $14.5 million (7.4% increase since May)

Vessel prices (values) have been rising since the beginning of the year, as several companies, such as Diana Shipping Inc. (DSX), have begun taking advantage of depressed price levels to purchase more ships in anticipation of a recovery in shipping rates in the near future.Fifteen-year-old vessel prices mirror shipping ratesShip prices (values) peaked in mid-2010, as supply growth started to outpace demand growth, driven by deliveries of a record number of ship orders placed before the financial crisis and lower year-over-year growth in dry bulk trade. As more fleets went unused, competition grew among firms, which pressured shipping rates and the overall profitability of shipping firms. Because companies can sell and purchase 15-year-old ships in the market right away—unlike new builds, which can take up to two years to construct—price movements in 15-year-old ships reflect nearer-term fundamentals than new build prices.Analysts expect shipping rates to rise from their current depressed levelThe recent rise in vessel price is another positive indicator of future supply and demand balance, which analysts expect to tighten. This would be positive for dry bulk companies such as DryShips Inc. (DRYS), Diana Shipping Inc. (DSX), Eagle Bulk Shipping Inc. (EGLE), Safe Bulkers Inc. (SB), and Navios Maritime Partnerships LP (NMM) over the medium to long term, because it suggests shipping rates will rise. Since several dry bulk companies have used ships as collateral to fund additional ship purchases in the past, higher ship values will also reduce the risk of violating loan covenants. 1 Learn more about the key performance indicators of the dry bulk shipping industryContinue to Part 11: New build prices, or go back to Part 1 to see the list of indicators.1. Loan covenants are activities that borrowers have agreed to carry out or not to carry out as part of the condition of receiving the loan. A violation of the loan (such as when the underlying value of a ship used to borrow more funds falls below a certain level) may give the creditor the right to ask for an early termination of a loan, which can lead to some serious financial problems for the borrower. Dry bulk shipping weekly analysis (Part 11: New build prices)Why new ship prices (values) matterAs we discussed in Part 10, ship prices reflect the current and future fundamentals of the shipping industry’s supply and demand balance. When market participants expect shipping rates to rise, shipping companies place more orders with ship construction companies, which drives prices for new ships higher. Apart from 15-year-old ship prices, it’s also important to track new build prices because they reflect the longer-term outlook of the dry bulk shipping industry’s fundamentals. This is because managers won’t pursue aggressive new purchases if they believe the short-term increase in rates won’t last.June’s Capesize vessel prices followed May’s jumpBased on the latest information available from Simpson Spence & Young, the world’s largest independent shipbroking group, prices for new-build Capesize vessels (the largest class of ships that mainly haul iron ore and coal across the ocean) in China stood at $47 million in June. This figure is unchanged from May but still follows a significant jump from $43 million per vessel in April. Ship prices have been falling since 2009, driven by the expectation of lower shipping rates due to large new orders. But the record increase in May, which sustained in June, shows managers have begun to purchase new ships in anticipation of higher Capesize shipping rates, along with a recovery in ship orders (see Part 2) and tighter supply and demand balance in the future.Capesize vessels could outperformAlthough prices for other ships (Panamax and Handymax or Supramax classes) are also showing turnarounds, they appear weaker compared to the gain we saw in Capesize prices. So this may indicate that companies with the largest exposure to Capesize vessels will perform better over the long run, likely driven by higher iron ore shipments as we’ve discussed in Part 7 and Part 8, as well as tighter supply additions. While this is positive for all dry bulk shipping companies—such as Diana Shipping Inc. (DSX), Safe Bulkers Inc. (SB), Navios Maritime Partners LP (NMM), Knightsbridge Tankers Ltd. (VLCCF), and DryShips Inc. (DRYS)—Knightsbridge Tankers Ltd. (VLCCF), with only Capesize vessels in its portfolio of ships, will benefit most.

Could construction activity be showing some signs of recovery?On August 9, the number of ships under construction as a percentage of existing vessels reversed a four-week decline, increasing from the prior week’s 4.26% to 4.34%. It’s too early to tell whether construction activity will continue to rise, but it’s a positive sign that higher shipping rates are nearer in sight—especially combined with the sharp declines in ship orders we saw in Part 2.Construction activity started rising in 2009, as shipbuilding firms began work on a large number of orders, which coincided with a peak in the number of ships ordered at ~50%. Activity has fallen since, because managers placed fewer orders post-2009, when they saw how much they’d over-ordered. Orders have continued to slip as ship construction firms worked through the large amount of ship orders. While managers have returned to the shipyard to place new orders, they haven’t needed the new ships immediately. As we’ve said in previous updates, the weakness in construction activity shows that managers are in no rush to receive these new orders and expect shipping rates as well as profitability to remain low for at least the short term. But last week’s data may just be the beginning of higher construction activity in the foreseeable future.Inference and outlookInvestors will be concerned that such an increase in construction activity may increase supply more than wanted in the future, which is why low construction activity could still have been positive for shipping companies. While that’s something to look out for (which stresses the importance for investors to look at several key indicators instead of just one) there’s a window of up to two years for that to occur, because of how long it takes to build a dry bulk ship.At the moment, we could take the recent data as neutral for dry bulk shipping companies such as DryShips Inc. (DRYS), Diana Shipping Inc. (DSX), Knightsbridge Tankers Ltd. (VLCCF), Eagle Bulk Shipping Inc. (EGLE), and Safe Bulkers Inc. (SB). As long as shipping rates continue to turn around, you may see higher construction activity as a positive. But if construction activity continues to rise without improvements in shipping rates, it will be negative.Dry bulk shipping weekly analysis (Part 4: Capacity growth)Why is capacity important?Although ship orders and construction activity are useful to get the insiders’ perspective, investors must also look at capacity growth to see whether it meets demand so that they don’t rely totally on managers, who can get caught up in the day-to-day operation without seeing the bigger picture. When capacity grows faster than demand, competition rises among individual shipping firms as they try to use idle ships and cover fixed costs. This lowers day rates, which negatively affects bottom line earnings, free cash flows, and share prices for companies. But when demand grows at a faster rate, it’s positive for dry bulk shippers.Annual capacity growth falls to a new lowOn August 2, dry bulk capacity, measured in deadweight tonnage (DWT, the weight a ship can safely carry across the ocean) and published weekly by IHS Global Limited, rose to 608.78 million DWT, while annual growth fell to a new low of 5.70%. Year-over-year growth using the last four weeks of data, which smooths out short-term noise, fell from 5.91% during the prior week to 5.83% this week.Driven by large placements of new ship orders, shipping capacity had a huge run over the past two years, as companies expected global trade growth to continue at a record. The recent decline in year-over-year capacity growth is a positive development because total dry bulk demand grew by just 5.1% during the first five months of 2013, as reported by RS-Platou, an international ship and offshore investment bank. Further growth in iron ore shipments coming out of Brazil and Australia due to capacity expansions (which we’ll discuss in later parts of this week’s update) as well as an expectation of a record grain output in the United States should lift demand higher towards the end of the year.Real test to come later this yearBut the real test will come later this year. Last year, several dry bulk shipping companies pushed back deliveries as China’s economic growth fell and shipping rates fell to a record low. The eight-week average weekly growth rate, shown in the chart above, fell to an average of 0.075%. Since the start of this year, capacity has grown ~4.08%. Unless we see the average weekly growth rate come down below 0.10%, capacity will likely grow by 7% this year, which could limit further upsides for dry bulk stocks such as Diana Shipping Inc. (DSX), Eagle Bulk Shipping Inc. (EGLE), Knigthsbridge Tankers Ltd. (VLCCF), Navios Maritime Partners LP (NMM), and DryShips Inc. (DRYS) until the end of this year. This could also harm medium-term share prices—especially if several maturing shipping contracts were drafted out above current market rates. Nonetheless, the current trend is positive for the industry’s long-term outlook. If investors stay focused on the favorable long-term prospects, dry bulk shipping companies will find support.Dry bulk shipping weekly analysis (Part 5: Electricity output)The significance of China’s industrial outputChina’s industrial output—crude steel and electricity outputs, to be specific—are bellwethers of demand for raw material shipments. When industrial production rises quickly, so does demand for raw materials like iron ore and coal, which often accompanies higher domestic production and imports. Since dry bulk ships take one to two years to construct, supply is quite inelastic. So changes in imports have large impacts on shipping rates, and vice versa.Industrial output rises highThe year-over-year change in China’s industrial output rose to 9.4% in July from 8.9% in June. Industrial output has fallen from last year’s December high of above 10% growth, when the government clamped down on soaring housing prices and shifted its stance towards lower economic growth in return for a more sustainable growth rate. But since second quarter GDP growth came in at exactly 7.5, the target the government set for the year, there’s an incentive for the government to increase public stimulus. This is likely what drove industrial output higher.Electricity output rises to a highFor the same month, electricity output rose to a high of 10.2% year-over-year growth—higher than June’s 8.1%% and a record since September 2011. Although electricity output doesn’t directly reflect crude steel production, it still depends on industrial activity that uses a lot of crude steel in constructing buildings and manufacturing cars. While the July update for crude output isn’t available, in China, most steel manufacturers are affiliated with the government. This means they have a responsibility to keep workers employed, or social unrest due to unemployment can create trouble. Plus, unless they’re losing significant money, companies have noted it’s often better to keep output constant rather than shut furnaces down only to restart them later. So it would be surprising if crude steel output falls substantially when we update it.Bulls and bearsInvestors have worried since a few months ago about whether the government’s move to cool the property market down would hurt industrial output. While the bulls will say industrial output continues to grow positively and hasn’t fallen off a cliff, the bears will point out that output growth isn’t as high as it was before. They’re both right. Compared to before the financial crisis, in 2010 and 2011, industrial output consistently stayed above 10% for steel and electricity output. This time around, though, growth reports have been lower, as the government’s not so eager to energize the economy by pumping more stimulus into it like it did before. This is because China’s transitioning to a consumption- and private enterprise–led economy. Just like how a job switch can be time-consuming and take some ramp-up time, the switch will take a while.Implication for shippingBecause share prices reflect the future outlook of a company’s earnings potential, lower output growth has negatively impacted share prices of shipping companies like DryShips Inc. (DRYS), Diana Shipping Inc. (DSX), Eagle Bulk Shipping Inc. (EGLE), Safe Bulkers Inc. (SB), and Navios Maritime Partners LP (NMM) in the short term. While China’s economic growth is unlikely to expand as fast as it once did, the market is starting to realize this, knowing that the world isn’t going to collapse. This will be positive for long-term share price movements driven more by long-term fundamentals.Dry bulk shipping weekly analysis (Part 6: Producer inflation)The significance of inflationAnalysts keep an eye on China’s inflation numbers because they show what policymakers may (or will) do with the country’s monetary policies. 1 When inflation rates are high, policymakers will tighten monetary policies to lower spending in the economy, which often slows down manufacturing activity. As China’s manufacturing activity is a key driver for dry bulk and oil trade, lower economic growth means lower revenues and earnings for shipping companies.Producer prices tick up in JulyConsumer price index (CPI) grew 2.7% in July—unchanged from June’s data. On the other hand, the year-over-year change in producer price index (PPI) rose to -2.3%—higher than June’s -2.7%. The consumer price index reflects the price of goods that consumers in China spend on average, whereas the producer price index reflects the wholesale prices received by domestic producers of goods and services.

Analysts widely consider the two indexes because a high inflation rate (although often suggesting strong demand and economic growth) will lower the purchasing power of money and lead to hyperinflation (extremely high inflation that’s gone out of control). This can lead to an economic collapse down the road, because either goods will become too expensive to purchase or money will become worthless. When money is worthless, the financial system collapses.Positive conclusion from low inflationJuly’s tame growth in the CPI was positive for monetary policy, while an uptick in PPI growth shows demand isn’t collapsing like it did in 2011. Because PPI is already near a cyclical low, if there’s a financial problem, the central bank can intervene to hold the economy from falling off the cliff. While cheap credit is definitely history, as China reins in on shadow banking activity—which Diana Shipping Inc. (DSX)’s CEO recently said in its second quarter earnings call—the probability that issues within China’s financial sector will spillover to other parts of the economy is quite limited.

This bodes positive for dry bulk shipping companies such as DryShips Inc. (DRYS), Diana Shipping Inc. (DSX), Navios Maritime Partners LP (NMM), Safe Bulkers Inc. (SB), and Knightsbridge Tankers Ltd. (VLCCF). A crash like the one we saw in 2008 is unlikely to happen.Learn more about indicators that drive the dry bulk industryContinue to Part 7: Australia’s exports or go back to Part 1 to see the list of indicators.1. Monetary policies are tools that central banks use to increase or decrease demand for loans through changes in the base interest rate or the bank’s ability to lend out money.Dry bulk shipping weekly analysis (Part 7: Australia’s exports)Australia: The commodity giantAustralia, one of the world’s most natural resource–rich countries, has become one of the largest commodity giants over the past decade, on the back of China’s golden age investment-led economic growth of 10% each year. Accounting for close to 50% of total iron ore shipments to China—as well as a percentage of total iron ore seaborne export—Australia’s iron ore export volume is a key indicator of dry bulk shipping demand. When Australia’s iron ore export volume grows at a rapid pace, it means more business for shipping companies, which bids up shipping rates. On the other hand, if export volume stagnates or falls, it will negatively affect shipping rates.Australia pushes ahead with larger exportAlthough the market has fallen due to China’s tolerance for lower economic growth since the start of the year and experts widely agree that China’s economy will never grow as fast as it did before the financial crisis, Australian iron ore producers haven’t slowed their production and shipments. Instead, they just exported a large amount (36.5 million metric tonnes) of iron ore in June—close to the record amount of 37 million metric tonnes of iron ore in May. The average iron ore import (using the last six months of data) rose from 33.4 million in May to 33.5 million in June. On a year-over-year basis, export rose by 30% (see the chart below).Capacity addition to support export volumesAnalysts predict export from Australia to increase further, as they expect the country to add approximately 100 million metric tonnes of capacity this year—half of which Rio Tinto will supply. That’s an extra 8 million per month. During the last quarter of 2013, Australia exported an average of ~45 million tonnes of iron ore per month. A maximum increase of 8 million tonnes of iron ore monthly should add roughly 17% annual growth to Australian iron ore exports towards the end of this year. In Diana Shipping Inc. (DSX)’s latest earnings call, it announced that it expects iron ore trade to increase by 10% in 2013.Since Australia’s iron ore export makes up ~13.5% of the world’s total dry bulk shipments, a 17% increase will add ~2.3% to global dry bulk shipping trade volume. This will have a positive impact on shipping rates—Capesize vessels in particular—which dry bulk shipping companies such as DryShips Inc. (DRYS), Diana Shipping Inc. (DSX), Knightsbridge Tankers Ltd. (VLCCF), Navios Maritime Partners LP (NMM), and Safe Bulkers Inc. (SB) will benefit from.Dry bulk shipping weekly analysis (Part 8: Shipping rates)Supply and demand drives dry bulk shipping companiesUnlike imports data that aren’t widely available on a weekly basis, shipping rates (which reflect the difference in supply and demand), are collected on a daily basis at the London-based Baltic Exchange and published as the Baltic Dry Indexes (BDI). These indexes reflect the daily shipping rates to transport key dry bulk raw materials in the spot market. When demand outpaces supply growth, shipping rates tend to rise. But when an increase in supply doesn’t meet with demand, shipping rates fall. 1 Lower rates in an uptrend Last week, the Baltic Dry Index fell from 1,065 on August 2 to 1,001 on August 9, dragged down by declines in Capesize and Panamax vessels. Excess supply growth in Panamax vessels continues to put downward pressure on rates. But current levels still stand higher than what they were for the most part of 2013. Shipping rates in the spot market have risen lately due to the lower capacity growth we saw in Part 4, the higher oil prices that shipping companies are passing on to customers, and increased iron ore trade from Australia (see Part 6) and Brazil.Higher imports have been driven by continuous growth in China’s steel output, a record-low inventory figure of ~57 million tons in March (a number unseen for three years), and a decline of ~$40 per metric tonne (28%) since the government began tightening the property market in February that has made imported iron ore more attractive. Capesize vessels, which primarily haul major bulk materials such as iron ore and coal, have benefited most.Future developmentBut as imported iron ore prices have risen to a recent high of $135.5 per metric tonne, the likelihood of lower iron ore imports has or will negatively impact rates in the near term. Nonetheless, investors expect iron ore prices to remain low as Australia and Brazil boost capacity, as we discussed in Part 6, by the end of this year, which would be positive for dry bulk shippers. Low inventories and continuous steel production China—despite what markets have feared—should help absorb the increase in supply. Plus, as U.S. rain improves prospects for a record corn output this year, analysts expect grain shipments to grow by 8% annually, likely to support Panamax rates.(Read more: Why the Baltic Dry Index has decoupled from the Chinese market)Shipping rates outlookIf the capacity trend we’ve seen in Part 4 continues to show improvements, we’ll likely end up seeing higher shipping rates in the second half of 2013 compared to the first half—a positive for companies such as Diana Shipping Inc. (DSX), Navios Maritime Partners LP (NMM), DryShips Inc. (DRYS), Knightsbridge Tankers Ltd. (VLCCF), and Safe Bulkers Inc. (SB).Learn more about the key performance indicators of the dry bulk shipping industryContinue to Part 9: Forward contracts, or go back to Part 1 to see the list of indicators.1. The two main revenue generation models in the shipping industry are spot (voyage) and time (period) charters. “Spot charters” refer to the one-time price of shipping a specific amount of raw material, while “time charters” reflect the price of borrowing a ship’s service for a specific period. “Time Charter Equivalent” (TCE), which converts spot charters (specified in $ per ton) to time charter rates ($ per day), is often used to compare companies in different markets. The two often mirror each other over the medium and long terms. Dry bulk shipping weekly analysis (Part 9: Forward rates) What are forward contracts?If there are shipping rates for today, then there’s also the expectation of tomorrow’s rates. Companies use forward contracts to lock in the availability of resources in the future at a set price. The dry bulk shipping industry—which transports key dry bulk materials such as iron ore, coal, and grain—is no exception to this practice. When shipping companies negotiate the rates of shipping raw materials, they consider future expected supply and demand. If the rate of renting a ship and service in a forward contract is higher than the current rate, it’s often a positive indication that shipping rates will rise. Higher shipping rates mean higher revenues, earnings, and free cash flows—and vice versa.Higher forward contract pricesAfter we saw forward contract charter rates for Capesize vessels (ships that mainly haul iron ore and coal) increase throughout the past few weeks, with the spread between the three tightening, all three contract rates (current quarter, forward one-year, and forward two-year) have pulled back on a weekly basis.Rates have all drifted lower over the past few years because shipbuilders delivered more than a necessary amount of newbuilds (new ships), driven by companies’ over-optimism toward future profitability. But since last year, shipping rates have started to base because several companies began to report negative earnings, capacity growth improved because of lower new ship deliveries, shipping companies continue to scrap older vessels, and shipment growth continues in dry bulk iron ore shipments.Unlike before 2010, when people in the industry expected new deliveries to continue to hurt future profitability, contracts that are farther into the future have priced above nearer-term rates for the past two years. This is happening because people in the industry expect supply growth to fall even farther in 2014 and 2015, as companies plan to allow the current excess capacity condition to alleviate and profitability to improve.Current rates rise above future ratesMore importantly, the current quarter’s time charter rates have now moved above rates for contracts that are farther into the future—something we’ve spoken of in prior articles. This reflects an unexpected increase in short-term demand. While this happened a few times in late 2011 and 2012, increases in one-year and two-year forward contracts didn’t exactly materialize back then. While we saw a decline in all three contracts, if we continue to see positive upward movement in forward one- and two-year rates, Capesize vessels should see a real recovery towards this end of this year.

With additional iron ore capacity coming out of Australia and Brazil, and China’s industrial output remaining positive, we could see positive surprises toward the end of this year in the dry bulk shipping industry. This bodes well for the long-term outlook of dry bulk shipping companies such as DryShips Inc. (DRYS), Diana Shipping Inc. (DSX), Safe Bulkers Inc. (SB), Navios Maritime Partners Inc. (NMM), and Knightsbridge Tankers Ltd (VLCCF), and the market will likely begin pricing them in over the next few months.Dry bulk shipping weekly analysis (Part 10: Ship prices) Why should you watch ship purchase prices?Purchase prices for ships are often good indicators of financial health in the shipping industry. When shipping demand grows more than the supply of ships, shipping companies place additional orders, which drives up purchase prices. Plus, when firms are able to charge higher prices for transporting goods across the ocean, profitability rises, and so does the value of ships.Panamax stabilizing, Handymax/Supramax risingDuring June, the average vessel prices for 15-year-old Panamax, Handymax/Supramax, and Handysize ships rose to a nine-month high.• Panamax: $9.5 million to $10.0 million (5.3% increase since May)

• Handymax/Supramax: $9.5 million to $10.0 million (5.3% increase since May)

• Handysize: $13.5 million to $14.5 million (7.4% increase since May)

Vessel prices (values) have been rising since the beginning of the year, as several companies, such as Diana Shipping Inc. (DSX), have begun taking advantage of depressed price levels to purchase more ships in anticipation of a recovery in shipping rates in the near future.Fifteen-year-old vessel prices mirror shipping ratesShip prices (values) peaked in mid-2010, as supply growth started to outpace demand growth, driven by deliveries of a record number of ship orders placed before the financial crisis and lower year-over-year growth in dry bulk trade. As more fleets went unused, competition grew among firms, which pressured shipping rates and the overall profitability of shipping firms. Because companies can sell and purchase 15-year-old ships in the market right away—unlike new builds, which can take up to two years to construct—price movements in 15-year-old ships reflect nearer-term fundamentals than new build prices.Analysts expect shipping rates to rise from their current depressed levelThe recent rise in vessel price is another positive indicator of future supply and demand balance, which analysts expect to tighten. This would be positive for dry bulk companies such as DryShips Inc. (DRYS), Diana Shipping Inc. (DSX), Eagle Bulk Shipping Inc. (EGLE), Safe Bulkers Inc. (SB), and Navios Maritime Partnerships LP (NMM) over the medium to long term, because it suggests shipping rates will rise. Since several dry bulk companies have used ships as collateral to fund additional ship purchases in the past, higher ship values will also reduce the risk of violating loan covenants. 1 Learn more about the key performance indicators of the dry bulk shipping industryContinue to Part 11: New build prices, or go back to Part 1 to see the list of indicators.1. Loan covenants are activities that borrowers have agreed to carry out or not to carry out as part of the condition of receiving the loan. A violation of the loan (such as when the underlying value of a ship used to borrow more funds falls below a certain level) may give the creditor the right to ask for an early termination of a loan, which can lead to some serious financial problems for the borrower. Dry bulk shipping weekly analysis (Part 11: New build prices)Why new ship prices (values) matterAs we discussed in Part 10, ship prices reflect the current and future fundamentals of the shipping industry’s supply and demand balance. When market participants expect shipping rates to rise, shipping companies place more orders with ship construction companies, which drives prices for new ships higher. Apart from 15-year-old ship prices, it’s also important to track new build prices because they reflect the longer-term outlook of the dry bulk shipping industry’s fundamentals. This is because managers won’t pursue aggressive new purchases if they believe the short-term increase in rates won’t last.June’s Capesize vessel prices followed May’s jumpBased on the latest information available from Simpson Spence & Young, the world’s largest independent shipbroking group, prices for new-build Capesize vessels (the largest class of ships that mainly haul iron ore and coal across the ocean) in China stood at $47 million in June. This figure is unchanged from May but still follows a significant jump from $43 million per vessel in April. Ship prices have been falling since 2009, driven by the expectation of lower shipping rates due to large new orders. But the record increase in May, which sustained in June, shows managers have begun to purchase new ships in anticipation of higher Capesize shipping rates, along with a recovery in ship orders (see Part 2) and tighter supply and demand balance in the future.Capesize vessels could outperformAlthough prices for other ships (Panamax and Handymax or Supramax classes) are also showing turnarounds, they appear weaker compared to the gain we saw in Capesize prices. So this may indicate that companies with the largest exposure to Capesize vessels will perform better over the long run, likely driven by higher iron ore shipments as we’ve discussed in Part 7 and Part 8, as well as tighter supply additions. While this is positive for all dry bulk shipping companies—such as Diana Shipping Inc. (DSX), Safe Bulkers Inc. (SB), Navios Maritime Partners LP (NMM), Knightsbridge Tankers Ltd. (VLCCF), and DryShips Inc. (DRYS)—Knightsbridge Tankers Ltd. (VLCCF), with only Capesize vessels in its portfolio of ships, will benefit most.