Pundits indicating that the dry bulk market’s sentiment remains weak

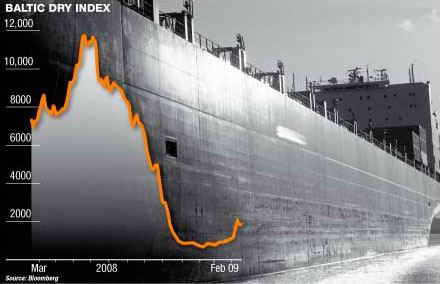

were justified, as the industry’s benchmark, the Baltic Dry Index (BDI)

kept falling mid-week, ending Wednesday’s session down by 1.47% to 1,411 points, the lowest it’s been since late of 2008, amid the global

financial meltdown. As has been the case since the beginning the year, smaller ship types fared better than their large counterparts.

Capesizes retreated yet again, this time by 0.88% very close to

break-even levels, while panamaxes ended the day down by 3.48%.

According to the latest weekly report from Fearnley’s, the Capesize market is lacking direction and excitement. «Finally we see the floor reached for now in the Far East, with a number of fixtures done around USD 6.65- 6.70 pmt for West Australia to China (against the lowest done last week at USD 6.45 pmt). The front haul seems under pressure, with lack of cargoes and more ballasters, and rates as dropping. The Chinese are preparing for lunar New Year, and remain inactive for the beginning of this year, resulting in limited spot activity” said the shipbroker.

Commenting on the panamax front, the report mentioned that it had a slow start to the week in both hemispheres. “Especially the Pacific market experienced low volumes with much of the Australian cargos being cancelled, caused by the flooding. Several ships were reported to leave the Australian loading areas without cargos, entering the much active ballasting market from the Pacific to the Atlantic basin. The latter has also experienced a softening in rates for early February cargos with ballast bonuses decreasing rapidly throughout the week. Fronthauls are still being fixed at around 25k and Tarvs at around 17.5k while the Pac rounds are getting around 9k. The period market has been over flooded with takers, but owners still not able/willing to face the levels being proposed” said Fearnley’s.

As for the smaller ship types and particularly the Handysize/Handymax, the shipbroker said that “negative sentiment for forward positions in the Atlantic market due to lack of cargo availability and too many ballasters from the East. Continued lack of sufficient activity in the Black Sea and Continent. USG seems to be the only positive market. Very little activity with rates having downward pressure across all routes in the Pac. Supras are doing USD 7-8k for Indonesia-India.

Same levels also seen for Thailand rounds. Iron ore from India bit quiet and vessels seeing around 14-15k from WCI and 10-11k from ECI for trip to East. RBCT coal FOB prices looking firm and not too many Indian buyers buying at those levels as cement plants have enough stocks for some time to hold. For RBCT RVs ships are going at 14k and some even lower depending on position. Handymax fertiliser cargoes from R.Sea to India are seen paying around low 20´s on voyage basis WCI discharge» concluded Fearnley’s.

Meanwhile, yesterday it was announced that Chinese coal imports set a new record in December and totaled 17.34 million tons, an increase of 940,000 tons (6%) from the previous record of 16.4 million tons imported in December 2009. Robust peak season winter thermal coal demand led to the surge in coal imports.In a relative comment, Commodore Research & Consultancy stated that “a few months ago we anticipated that Chinese coal imports would set a new record in December and published a note in early November alerting clients that December coal imports would likely reach 17.25 million tons.

December imports exceeded our forecast partially due to Chinese ports being closed sporadically in November due to weather-related issues. A few cargoes that were meant to be unloaded in November were instead unloaded in December.

Going forward, Chinese coal imports are likely to remain at robust levels but are poised to decline until the summer re-stocking period. Chinese thermal coal fixtures have declined in recent weeks. Last week saw only 6 vessels chartered to ship thermal coal to China, a decrease from the trailing four-week average of 9 fixtures. Early December saw as many as 19 vessels chartered to ship thermal coal to China in a single week” said Commodore.

According to the latest weekly report from Fearnley’s, the Capesize market is lacking direction and excitement. «Finally we see the floor reached for now in the Far East, with a number of fixtures done around USD 6.65- 6.70 pmt for West Australia to China (against the lowest done last week at USD 6.45 pmt). The front haul seems under pressure, with lack of cargoes and more ballasters, and rates as dropping. The Chinese are preparing for lunar New Year, and remain inactive for the beginning of this year, resulting in limited spot activity” said the shipbroker.

Commenting on the panamax front, the report mentioned that it had a slow start to the week in both hemispheres. “Especially the Pacific market experienced low volumes with much of the Australian cargos being cancelled, caused by the flooding. Several ships were reported to leave the Australian loading areas without cargos, entering the much active ballasting market from the Pacific to the Atlantic basin. The latter has also experienced a softening in rates for early February cargos with ballast bonuses decreasing rapidly throughout the week. Fronthauls are still being fixed at around 25k and Tarvs at around 17.5k while the Pac rounds are getting around 9k. The period market has been over flooded with takers, but owners still not able/willing to face the levels being proposed” said Fearnley’s.

As for the smaller ship types and particularly the Handysize/Handymax, the shipbroker said that “negative sentiment for forward positions in the Atlantic market due to lack of cargo availability and too many ballasters from the East. Continued lack of sufficient activity in the Black Sea and Continent. USG seems to be the only positive market. Very little activity with rates having downward pressure across all routes in the Pac. Supras are doing USD 7-8k for Indonesia-India.

Same levels also seen for Thailand rounds. Iron ore from India bit quiet and vessels seeing around 14-15k from WCI and 10-11k from ECI for trip to East. RBCT coal FOB prices looking firm and not too many Indian buyers buying at those levels as cement plants have enough stocks for some time to hold. For RBCT RVs ships are going at 14k and some even lower depending on position. Handymax fertiliser cargoes from R.Sea to India are seen paying around low 20´s on voyage basis WCI discharge» concluded Fearnley’s.

Meanwhile, yesterday it was announced that Chinese coal imports set a new record in December and totaled 17.34 million tons, an increase of 940,000 tons (6%) from the previous record of 16.4 million tons imported in December 2009. Robust peak season winter thermal coal demand led to the surge in coal imports.In a relative comment, Commodore Research & Consultancy stated that “a few months ago we anticipated that Chinese coal imports would set a new record in December and published a note in early November alerting clients that December coal imports would likely reach 17.25 million tons.

December imports exceeded our forecast partially due to Chinese ports being closed sporadically in November due to weather-related issues. A few cargoes that were meant to be unloaded in November were instead unloaded in December.

Going forward, Chinese coal imports are likely to remain at robust levels but are poised to decline until the summer re-stocking period. Chinese thermal coal fixtures have declined in recent weeks. Last week saw only 6 vessels chartered to ship thermal coal to China, a decrease from the trailing four-week average of 9 fixtures. Early December saw as many as 19 vessels chartered to ship thermal coal to China in a single week” said Commodore.