According to observers the dry bulk freight market has been supported to some considerable extent by hefty volumes of iron ore being shipped to China although the significant gains are likely to subside in the coming weeks.

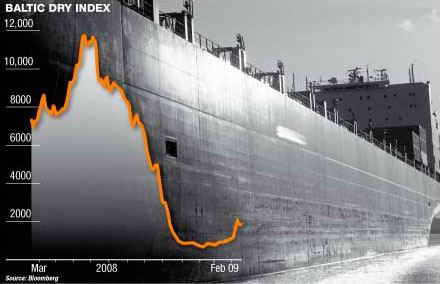

According to shipbroker data the Baltic Dry Index which tracks global dry bulk shipping rates has risen by some 70% since the beginning of August hitting a 10 month high of 2,173 points on Friday. The BDI has already lost some ground in the current week sliding to 2,136 on Tuesday. Front quarter capesize prices on the freight derivatives market meanwhile dropped for the first time this month to USD 23,875/day at Tuesday close compared with USD 24,000 per day on Monday and around USD 18,000 per day in early October.

Mr Jeffery Landsberg MD of New York based analysts Commodore Research & Consultancy said the capsize market which has largely been driving the BDI rise in recent weeks is already showing signs of imminently bearish factors. He said that “Chinese iron ore production has remained robust which is putting pressure on global iron ore prices and Chinese iron ore fixture volumes this week.”

He added that “Chinese steel prices have continued to decline this week. If prices continue to decrease and stockpiles stay high, near term Chinese steel production would remain likely to suffer a decline. But others are less immediately bearish, albeit for just the shorter term.”

Mr Miswin Mahesh Barclays Capital analyst said “Despite the ongoing worries concerning the expansionary state of the dry bulk fleet, the BDI has produced stellar gains since August, driven primarily by demand for capesize vessels to carry iron ore cargo bound to China.”

He said “In the very short term, the recent softening of international iron ore prices bodes well for seaborne trade and volumes bound to China in particular are likely to pick up in the coming weeks given the attractive differential with domestic iron ore prices in the country.”

Mr Mahesh said. “However, despite this current preference towards imported iron ore, the actual requirement for iron ore itself is likely to come under pressure in the near term given that demand from the ultimate downstream consumer of steel is showing signs of moderation.”

He added that Capesize vessels are more than 100,000 deadweight tonnes and largely operate on long-haul coal and iron ore trade routes.