“Since ordering momentum continues, due in large part to a feeling that the market is coming off of cycle lows, the threat of vessel oversupply looms. However, the uptick in ton-mile demand could offset the incremental new tonnage supply in the near term,”according to Poten & Partners.

The current order book for tankers, 30,000 deadweight and larger, is 66.1 million deadweight tons (mDWT) through 2017.

However, the reported new orders do not account for the differential between the January 2014 order book and that of today.

At the start of the year, the 2014 order book was 27.2 mDWT, the current order book is 15.9 mDWT and only 8.1 mDWT has reportedly delivered. This differential suggests that 3.3 mDWT, or 12%, of the originally reported order book is on a surface level unaccounted for.

As explained by the report, these vessels are likely to have simply slipped into later years. Looking at the year-to-date delivery pace, this could explain for the majority of that differential.

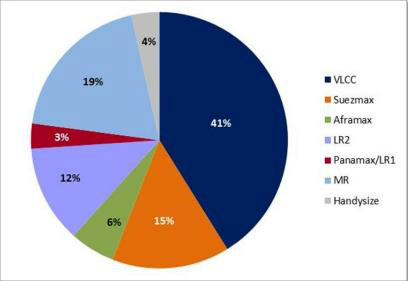

The bulk of the order book, 41% is made up of VLCC tonnage, the majority of which is currently slated to deliver in 2016. As of the beginning of August, 11 VLCCs have been delivered of an initially expected 36. At this rate, the total deliveries for full year 2014 will be 20 vessels; 16 VLCCs have slipped forward, or been renegotiated and or cancelled.

For example, speculation surrounding the ultimate deliverability of the Suezmax order book is a function of both shipyard capability and orderer of record. Some schools of thought speculation surrounding the ultimate deliverability of the Suezmax order book is a function of both shipyard capability and orderer of record,” the report reads.“On a sector-by-sector basis, a thorough review of credit risk from the shipowner and shipyard perspective can help to hone the view on the actual new supply expected.

Some believe that the Suezmax order book is realistically only 55% of the 62 vessels reportedly on order, suggesting that widely reported order book numbers grossly overstate the reality of new tonnage supply in the next few years.

While shipyard statistics is sometimes a pseudoscience, shipowners are still cautioned not to over-do the ordering in the grander sense.

“Although, for many, it is still difficult to forget the glut of tonnage that has largely plagued the market for most of the past decade, group-think is a powerful force.

Today’s freight environment suggests the faint hope of light at the end of the tunnel, but any rapid influx of tonnage could seriously hinder the upside in earnings for the longer-term,” Poten & Partners concludes.