Ocean carriers were again unable to make any of their GRIs between Asia and the Indian Subcontinent/Mid-East region stick in 4Q 13.

Westbound

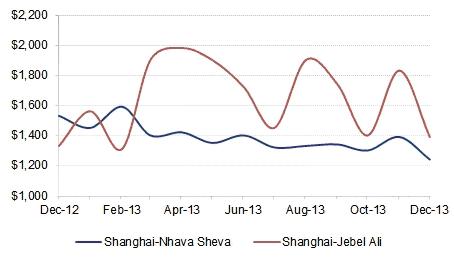

Ocean carriers continued to struggle with sub-economic freight rate levels between Asia and the Indian Subcontinent/Middle East region (MEISC) in the last quarter of 2013 due to insufficient vessel capacity being withdrawn in a declining market. As explained in ‘Supply-Demand’, no services were merged or taken out, only sailings cancelled, contributing to the westbound pricing volatility shown in Figure 7. As surrounding vessels filled up, rates briefly increased, and vice versa.

According to Drewry’s Container Freight Rate Insight, all-in freight rates quoted to forwarders for spot cargo from China (Shanghai) to the West Coast of India (Nhava Sheva) continued to oscillate between $1,400/40ft and $1,350/40ft up to the end of November, and then dipped down to $1,240/40ft in December. The fluctuation from Shanghai to Jebel Ali was even wilder, ranging between $1,900/40ft and $1,400/40ft up to November, before falling further to $1,390/40ft in December. Market sources say that even lower rates were available.

Figure 7

Drewry CFRI Westbound Asia to MidEISC Spot Rates (US$/40ft)

Source: Drewry Container Freight Rate Insight (www.drewry.co.uk/cfri)

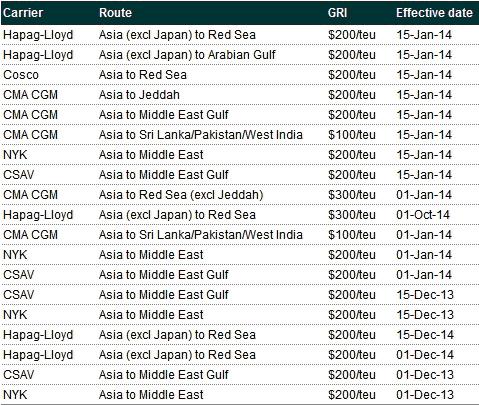

A further factor in the volatility was the regular attempts by carriers to impose GRI’s, which resulted in rates shooting on the prescribed date, only to fall back shortly afterwards due to lack of faith. Figure 7a shows the latest GRIs, revealing that another two were already due to be implemented in January this year.

Table 2

Recent GRIs Between Asia and MEISC

Source: Drewry Maritime Research

Ocean carriers specialising in the tradelane have also been hampered by lower freight rates offered by transhipment service providers deploying empty ships on their way from Asia to Europe. Although the total trade between Asia and MEISC remained unchanged between January and November compared to the same period in 2012, at just over 8 million teu, Colombo’s transhipment cargo from all trades grew by a much greater 12.3% in 2013, up 1,779,882 teu (all trades), indicating some success on the part of indirect service providers. Some of this might have been at the expense of other hubs, however.

The market is largely controlled by forwarders, who know better than most how to play direct and indirect service providers off against each other – even those carriers now calling directly at Mid-East Gulf ports other than Jebel Ali. They also know well how to undermine ocean carrier GRI initiatives.

Eastbound

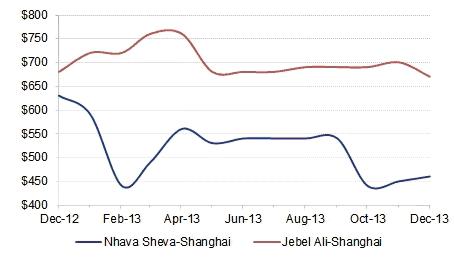

Freight rates also remained at sub-economic levels from the MEISC region back to Asia during the final quarter of last year. According to Drewry’s CFRI, the average all-in price quoted to forwarders for spot cargo from Jebel Ali to Shanghai remained at just under $700/40ft, whilst that from Nhava Sheva to Shanghai fell from $540/40ft to $450/40ft (see Figure 8).

Figure 8

Drewry CFRI Eastbound Asia to MidEISC Spot Rates (US$/40ft container)

Source: Drewry Container Freight Rate Insight (www.drewry.co.uk/cfri)

Source: Drewry Container Freight Rate Insight (www.drewry.co.uk/cfri)

With eastbound trade falling by 13% between January and November, the shortage of cargo was worse than normal, and the only thing ocean carriers could hope for was a contribution towards repositioning costs. At these rate levels there is no money to pay for empty positioning, so where exports exceeded imports, better rates were available.

Our View

Westbound freight rates to the MEISC region should increase in 1Q 14 due to increased seasonal cargo and less competition from Asia-Europe services. However, until the over-supply of vessel capacity is addressed through the formation of bigger consortia or alliances, these routes have little chance of operating economically.

Westbound

Ocean carriers continued to struggle with sub-economic freight rate levels between Asia and the Indian Subcontinent/Middle East region (MEISC) in the last quarter of 2013 due to insufficient vessel capacity being withdrawn in a declining market. As explained in ‘Supply-Demand’, no services were merged or taken out, only sailings cancelled, contributing to the westbound pricing volatility shown in Figure 7. As surrounding vessels filled up, rates briefly increased, and vice versa.

According to Drewry’s Container Freight Rate Insight, all-in freight rates quoted to forwarders for spot cargo from China (Shanghai) to the West Coast of India (Nhava Sheva) continued to oscillate between $1,400/40ft and $1,350/40ft up to the end of November, and then dipped down to $1,240/40ft in December. The fluctuation from Shanghai to Jebel Ali was even wilder, ranging between $1,900/40ft and $1,400/40ft up to November, before falling further to $1,390/40ft in December. Market sources say that even lower rates were available.

Figure 7

Drewry CFRI Westbound Asia to MidEISC Spot Rates (US$/40ft)

Source: Drewry Container Freight Rate Insight (www.drewry.co.uk/cfri)

A further factor in the volatility was the regular attempts by carriers to impose GRI’s, which resulted in rates shooting on the prescribed date, only to fall back shortly afterwards due to lack of faith. Figure 7a shows the latest GRIs, revealing that another two were already due to be implemented in January this year.

Table 2

Recent GRIs Between Asia and MEISC

Source: Drewry Maritime Research

Ocean carriers specialising in the tradelane have also been hampered by lower freight rates offered by transhipment service providers deploying empty ships on their way from Asia to Europe. Although the total trade between Asia and MEISC remained unchanged between January and November compared to the same period in 2012, at just over 8 million teu, Colombo’s transhipment cargo from all trades grew by a much greater 12.3% in 2013, up 1,779,882 teu (all trades), indicating some success on the part of indirect service providers. Some of this might have been at the expense of other hubs, however.

The market is largely controlled by forwarders, who know better than most how to play direct and indirect service providers off against each other – even those carriers now calling directly at Mid-East Gulf ports other than Jebel Ali. They also know well how to undermine ocean carrier GRI initiatives.

Eastbound

Freight rates also remained at sub-economic levels from the MEISC region back to Asia during the final quarter of last year. According to Drewry’s CFRI, the average all-in price quoted to forwarders for spot cargo from Jebel Ali to Shanghai remained at just under $700/40ft, whilst that from Nhava Sheva to Shanghai fell from $540/40ft to $450/40ft (see Figure 8).

Figure 8

Drewry CFRI Eastbound Asia to MidEISC Spot Rates (US$/40ft container)

Source: Drewry Container Freight Rate Insight (www.drewry.co.uk/cfri)With eastbound trade falling by 13% between January and November, the shortage of cargo was worse than normal, and the only thing ocean carriers could hope for was a contribution towards repositioning costs. At these rate levels there is no money to pay for empty positioning, so where exports exceeded imports, better rates were available.

Our View

Westbound freight rates to the MEISC region should increase in 1Q 14 due to increased seasonal cargo and less competition from Asia-Europe services. However, until the over-supply of vessel capacity is addressed through the formation of bigger consortia or alliances, these routes have little chance of operating economically.