Mediterranean imports from Asia are said to be rising impressively, encouraging carriers to impose swinging freight rate increases, but exceptional circumstances are probably responsible.

Westbound

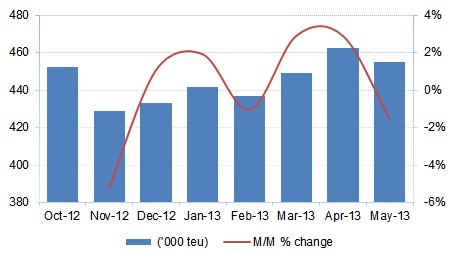

Cargo from Asia to the Mediterranean improved significantly in April, jumping from a monthly average of 366,000 teu in the first quarter to 401,000 teu. The 10% increase is surprising, as economic conditions in the Mediterranean remained dire, with many countries, such as Spain, Italy, Greece and France, still in recession. Overall growth in the first four months of the year was still only 1.8% year-on-year.

The rise in April was evenly split between the Western Mediterranean/North Africa region and the Eastern Mediterranean/Black Sea region, which suggests that it might only be seasonal.

It is possible that, with so much industrial and political unrest seething in the region – most recently in Turkey – importers have decided to get their merchandise in well ahead of the peak season as a precaution. Not that last year’s summer was anything to get excited about. Between June and September, exports from Asia actually fell by 1.6%, compared to the previous four month period. The peak season usually comes around a month earlier than in Northern Europe due to the importance of tourism.

Westbound Asia-Mediterranean Container Traffic (’000 teu)

Source: Drewry Maritime Research, derived from CTS

Source: Drewry Maritime Research, derived from CTSOcean carriers’ response was to leave their schedules well alone. Only three sailings were cancelled in April, compared to seven in March, which was then increased back to seven in May. Otherwise, only vessel upgrades and port pair changes continued to be made. It was strongly rumoured that the G6 planned to withdraw its ABX service into the Baltic Sea, but it never happened. According to a source within one of the partner lines, the schedules’ berthing windows are precious to lose lightly.

The consequence is that westbound vessel capacity grew by 2.9% between March and April, up to 461,995 teu, which was followed by a 1.6% reduction in May, back to 454,774 teu.Westbound Asia to Mediterranean Capacity (’000 teu)

Source: Drewry Maritime Research, derived from CTS

Source: Drewry Maritime Research, derived from CTSThe uncharacteristic scheduling inactivity might be explained by last week’s bombshell from Maersk Line, MSC and CMA CGM that joint east-west services have been being planned over the past six months, for implementation in 2Q 14. The three intend to operate within an alliance called P3. In the case of the tradelane between Asia and the Mediterranean, five strings will be provided, which is the same as at present. Maersk and CMA CGM offer the AE11/MEX1, AE20/MEX3 and AE3/BEX services, and MSC offer the Dragon and Tiger services.

The P3 deal, which also includes the transpacific and transatlantic tradelanes, is still subject to regulatory approval, which will be interesting in the Mediterranean as Maersk/MSC/CMA CGM’s share of effective vessel capacity (ie after allowing for wayporting and transhipment etc) from Asia was a hefty 51% in May, well above the limit of 30% recommended in the EU’s consortia regulations.If approved by the European Commission, it is not hard to imagine Daily Maersk being extended to certain ports in the Mediterranean. On the other hand, if the P3 alliance is accused by shippers of abuse of a dominant position, it will have to demonstrate that the efficiencies brought about by the cooperation outweigh the harm to competition.

The consequence of the inactivity in schedule changes and 10% increase in cargo resulted in the average utilisation of all vessels sailing from Asia to the Mediterranean rising from a poor 81% in March to 87% in April. Although healthy, it was not enough to stop freight rates continuing to plummet (see figure below), as described in the next section on pricing, and in ‘Mind over matter’ (see CIW dated 17 June). Industry feedback indicates that May’s average vessel utilisation was even.

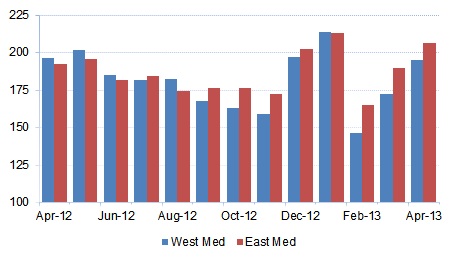

Westbound Asia-Mediterranean Utilisation v Rates

Sources: Drewry Maritime Research; World Container Index assessed by Drewry

Sources: Drewry Maritime Research; World Container Index assessed by Drewry Eastbound

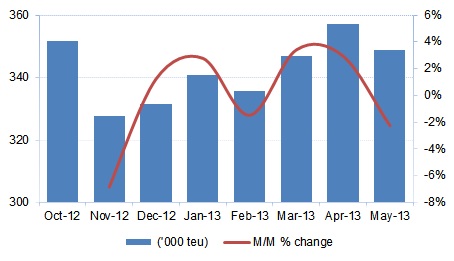

Exports from the Mediterranean to Asia declined by 4% between March and April, down to 167,000 teu, due to a 9% decline from the Western region and North Africa, to 85,000 teu. Exports from the Eastern Mediterranean and Black Sea rose by just over 1%, to 82,000 teu. The total for the first four months of the year was still 9% higher than in the same period of 2012, never-the-less.

Although eastbound trade is at best marginal, the growth is important in helping to diminish the chronic container equipment imbalance in the region. Compared to the 1,500,000 teu imported from Asia in the first four months of the year, only 654,000 teu were exported back, which means that ocean carriers continued to be stuck with high empty repositioning costs.

It is not yet clear to what extent Japan’s 20% currency devaluation in March has put a dampener on its imports from the Mediterranean. During the first three months of the year, the value of the traffic represented just 2.6% of Japan’s total imports.

The same applies to China’s ‘Green Fence’ regulation, which aims to clean up the quality of recyclable waste imports, a major mover in containers from Europe.

Eastbound Asia-Mediterranean Container Traffic (’000 teu)

Source: Drewry Maritime Research, derived from CTS

Source: Drewry Maritime Research, derived from CTSDue to the westbound schedule changes and vessel cancellations mentioned earlier, eastbound vessel capacity increased by 2.9% between March and April, up to 356,916 teu, but then fell back by 2.3% in May, down to 348,817 teu.

Eastbound Mediterranean to Asia Capacity (’000 teu) Source: Drewry Maritime Research

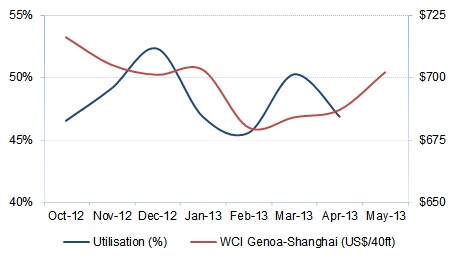

The consequence is that the average utilisation of all vessels sailing

back to Asia from the Mediterranean fell from a paltry 50% in March to

just 47% in April, so it is unsurprising that freight rate levels for

spot cargo continued to languish between $650/40ft and $700/40ft. (see

next section on Pricing for further details)

Source: Drewry Maritime Research

The consequence is that the average utilisation of all vessels sailing

back to Asia from the Mediterranean fell from a paltry 50% in March to

just 47% in April, so it is unsurprising that freight rate levels for

spot cargo continued to languish between $650/40ft and $700/40ft. (see

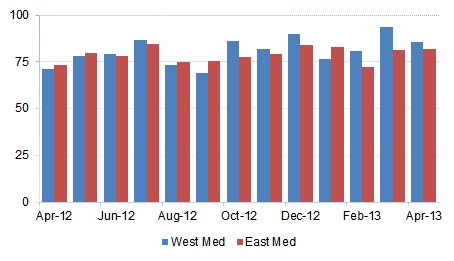

next section on Pricing for further details)Eastbound Asia-Mediterranean Utilisation v Rates

Research; World Container Index assessed by Drewry

Research; World Container Index assessed by Drewry Asia-Mediterranean – estimated monthly supply/demand position

, Notes:

*After deduction of 20% eastbound and 8.5% westbound for unusable slots

due to deadweight limitations and high-cube adjustment, plus further

deduction for out-of scope cargoes 2.5% eastbound and 2.0% westbound

Source: Drewry Maritime Research

Recent cargo growth from Asia to the Mediterranean is most probably seasonal, and will not last long. The need for vessel capacity reduction has only been postponed, therefore.