In July 1969 The Rolling Stones played a concert in Hyde Park and last

week, 44 years later, they were back. "Were any of you here in 1969?"

Mick Jagger asked the crowd and quite a few were. But in 1969 a lot of

the crowd couldn’t hear much because the amps were so feeble and there

were no screens. Today rock concerts have moved on; the technology is

stunning and so is the band, despite their wrinkles.

Vintage Year For VLCCs

On the subject of historic gigs, this summer is the 40th anniversary of

the 1973 tanker boom, the closest shipping has got to a rock festival.

During the few months it lasted, shipping’s own heavy metal band, the

VLCCs, gave a historic performance. The event got off to a slow start in 1972, but when the VLCC band tuned up in 1973, they were red hot. They

opened with WS 260 in June, followed by WS 296 in August, WS 342 in

September, and did WS 334 for the finale in October.

On the subject of historic gigs, this summer is the 40th anniversary of

the 1973 tanker boom, the closest shipping has got to a rock festival.

During the few months it lasted, shipping’s own heavy metal band, the

VLCCs, gave a historic performance. The event got off to a slow start in 1972, but when the VLCC band tuned up in 1973, they were red hot. They

opened with WS 260 in June, followed by WS 296 in August, WS 342 in

September, and did WS 334 for the finale in October.

What Were They Smoking?

This was new territory and the punters went berserk. Tanker orders poured in, adding 105m dwt to the orderbook (60% of the fleet). But on 6th October the Egypt-Israel war started and the music stopped. Two weeks later OPEC cut oil production by 5%, and oil shot to $12/bbl. The festival fizzled out and the players went home, nursing a massive hangover.

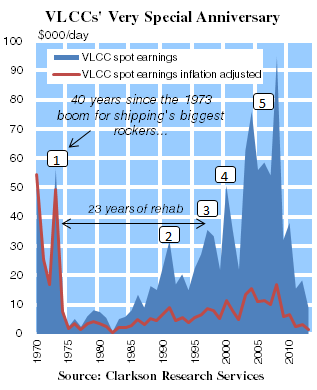

They were heading for one of the toughest recessions in history. Earnings crashed from $54,000/day in 1973 to $2,400/day in 1975. Timecharter income ran out, LIBOR hit 16% in 1981 and crude oil trade fell by 30%. The graph shows earnings since then on a nominal and inflation adjusted basis, numbering the peaks. By 1983 modern VLCCs sold for $3m and in 1986 were still earning $6,000/day. It took another decade to get back to normal. During the mini-peak (2) in 1991 earnings edged up to $31,000/day, but after inflation they remained weak. Finally the 1997 peak (3) signalled the hidden surplus was gone and it was “back to normal”. In the 2000s (4 and 5) even better markets arrived but in inflation adjusted terms the best they managed was $16,935/day in 2008.

Yet through all this, investment continued. Between 1974 and 1996, 200m dwt of tankers were ordered. The lesson is that shipping cycles are not just about selfcontained peaks and troughs. The effect of major disruptions can be so drawn out that players start to think of them as the norm. However bad the disruption, business goes on: cargo moves, mini-booms happen, and new ships get ordered, even if profits remain scarce.

Wrinkles for Today’s Investors

So, tanker investors grew their fleet by 75% between 1972 and 1977 and then got unlucky. Demand went wrong and they spent the next 20 years squeezing out the surplus. More recently, the bulker fleet grew by 78% between 2006 and 2012, but so far demand and interest rates are OK. Investors will hope history doesn’t always repeat itself. Have a nice day

Vintage Year For VLCCs

On the subject of historic gigs, this summer is the 40th anniversary of

the 1973 tanker boom, the closest shipping has got to a rock festival.

During the few months it lasted, shipping’s own heavy metal band, the

VLCCs, gave a historic performance. The event got off to a slow start in 1972, but when the VLCC band tuned up in 1973, they were red hot. They

opened with WS 260 in June, followed by WS 296 in August, WS 342 in

September, and did WS 334 for the finale in October.What Were They Smoking?

This was new territory and the punters went berserk. Tanker orders poured in, adding 105m dwt to the orderbook (60% of the fleet). But on 6th October the Egypt-Israel war started and the music stopped. Two weeks later OPEC cut oil production by 5%, and oil shot to $12/bbl. The festival fizzled out and the players went home, nursing a massive hangover.

They were heading for one of the toughest recessions in history. Earnings crashed from $54,000/day in 1973 to $2,400/day in 1975. Timecharter income ran out, LIBOR hit 16% in 1981 and crude oil trade fell by 30%. The graph shows earnings since then on a nominal and inflation adjusted basis, numbering the peaks. By 1983 modern VLCCs sold for $3m and in 1986 were still earning $6,000/day. It took another decade to get back to normal. During the mini-peak (2) in 1991 earnings edged up to $31,000/day, but after inflation they remained weak. Finally the 1997 peak (3) signalled the hidden surplus was gone and it was “back to normal”. In the 2000s (4 and 5) even better markets arrived but in inflation adjusted terms the best they managed was $16,935/day in 2008.

Yet through all this, investment continued. Between 1974 and 1996, 200m dwt of tankers were ordered. The lesson is that shipping cycles are not just about selfcontained peaks and troughs. The effect of major disruptions can be so drawn out that players start to think of them as the norm. However bad the disruption, business goes on: cargo moves, mini-booms happen, and new ships get ordered, even if profits remain scarce.

Wrinkles for Today’s Investors

So, tanker investors grew their fleet by 75% between 1972 and 1977 and then got unlucky. Demand went wrong and they spent the next 20 years squeezing out the surplus. More recently, the bulker fleet grew by 78% between 2006 and 2012, but so far demand and interest rates are OK. Investors will hope history doesn’t always repeat itself. Have a nice day