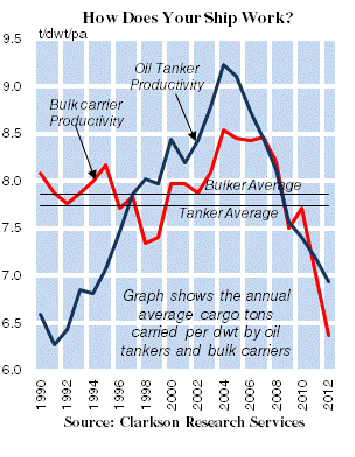

Dip, dip, dip my little ship sails on the ocean, you are it! It’s just a children’s counting out rhyme, but in the Monty Python Black Eagle sketch its purpose was to choose one person who had to take the “other” way out, because there were not ample rations to go round. Simple enough, until the Major was “it” and did not want to play any more. What is “It”? The question of who is to be “it” also taxes a shipping industry where there are plenty of vessels but also limited rations, in the form of cargoes, to go round, and earnings are at rock bottom. Scrapping is not having much of an impact on supply and, as we asked last week, where’s the lay-up? “It” appears to be the hit being taken by productivity, as depicted in our Graph of the Week. It shows cargo tonnes carried per dwt per annum by bulk carriers and oil tankers over the last two decades, along with their long period averages.

Tankers Work Rate Up and Down

For oil tankers, productivity was at its lowest in the early 1990s when the first Gulf War impacted on their performance. But in the nine years 1994-2003 hardly any growth in the fleet, but a 30% increase in trade, meant they had to work much harder (or smarter?) and productivity soared to over 9 t/dwt pa. During the next nine years to 2012 trade expanded by a further 19%, but the fleet by more than 50%. Productivity of the fleet slipped back to 7 t/dwt pa.

Bulkers Bumble Along

Productivity of the bulk fleet bumbled along up to 2008 pretty much in line with the economic cycles of the period, as both the fleet and trade grew at similar rates. The rapid expansion of trade to China clearly required bulk carriers to work a bit harder and their productivity rose to 8½ t/dwt pa over 2004-07. Unfortunately, the rush of ships thereafter saw capacity grow at almost three times the rate of cargoes and the productivity of the bulk fleet shrunk to under 6½ t/dwt pa.

Work Differently, Not Harder

With our measure of productivity dipping so low, why is unemployment (lay-up) not higher? It’s a question currently taxing economists in a more general sense, and the answer is similar for shipping i.e. that ships are working differently (if not harder). Economic slow steaming is clearly a major influence reducing vessels’ productivity; but so are extended periods waiting for or loading cargoes. Not an issue, however, are longer trade hauls, since growth in tonne-miles has not been noticeably greater than growth in tonnes.

Doldrums, Not Dole…

So, there you have it. Shipping is heading for the doldrums if not for the dole queue. With too many ships, and still more to come, the growth of cargo volumes is the long term hope for the future. However, the dip, dip, dip of growth in the European, American and Chinese economies does not bode well for demand in the short term. Maybe it’s time to bite the bullet and go for an “other” way out.