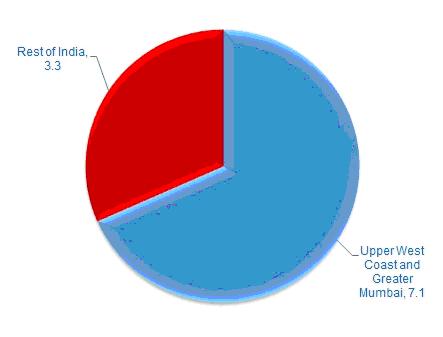

The easing of tariff regulation in India’s major ports since last year is already attracting new investment and should help address the chronic capacity shortage, particularly in its largest container gateway, Jawaharlal Nehru Port (JNP). Ocean carriers will be watching this situation closely, as the easing of congestion in JNP would enable a number of significant schedule improvements to be made. Ports in India’s Upper West Coast and in the Greater Mumbai area account for two thirds of the country’s container volume, and despite its congestion and limitations, JNP remains the biggest port in the country by some margin.

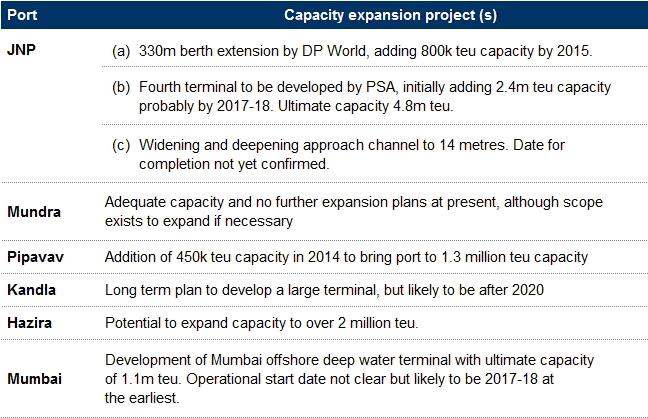

Take away its congestion, and ocean carriers would no longer have to worry about vessels being delayed there before going on to other countries.In this respect, the port has seen two key events in the last few weeks – firstly the laying of the foundation stone for the expansion of capacity by 800,000 teu by DP World, with rapid completion targeted for 2015, and secondly the approval of PSA as winning bidder for the development of a huge new terminal at the port, with an ultimate capacity of 4.8 million teu p.a. – more than double the port’s present 4.1 million teu capacity. The PSA announcement is particularly noteworthy given that the company was previously part of a successful joint venture bid for this project before negotiations broke down amongst legal acrimony.Significant in this context is the recent decision by the Indian Government to partially relax the strict tariff regulation which applies to terminals in its designated major public ports. The PSA project will likely be the first to benefit from this.

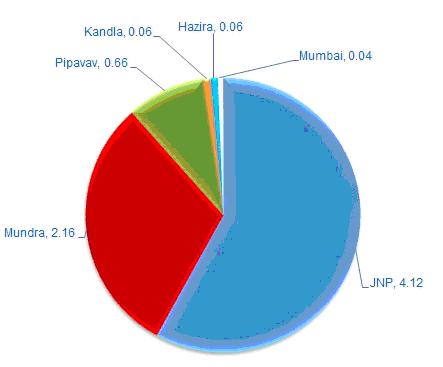

The more relaxed rules will allow terminal operators to raise their tariffs every year based on market conditions (subject to a cap of 15%) provided agreed performance standards are met. This change should make investment in terminals in the major ports more viable and less risky, and help accelerate the addressing of congestion and capacity shortages. For a while it looked like existing terminals in the major ports would have to continue to live with the full tariff regulation as the change was not retrospective, but a recent move looks likely to ensure a level playing field.Private ports like Mundra and Pipavav, just up the coast, have always been outside the central Government tariff regulation scheme, and this is one factor that has allowed them to grow at the expense of the likes of JNP, along with having deeper water and available capacity. Volumes at Mundra for example increased by 28% in 2013 to over 2 million teu making it the country’s second largest container port. It has an estimated deep water capacity of 3.6 million teu p.a. and now includes a joint venture terminal with TIL (MSC).

Figure 1 Regional Split, Indian Container Port Traffic, 2013 (M teu) Source: Drewry Maritime Research

Source: Drewry Maritime Research

Figure 2 Upper West Coast and Greater Mumbai: Volumes by Port, 2013 (M teu) Source: Drewry Maritime Research

Source: Drewry Maritime Research

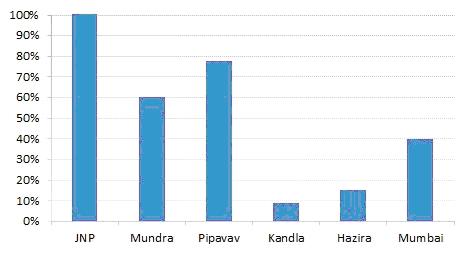

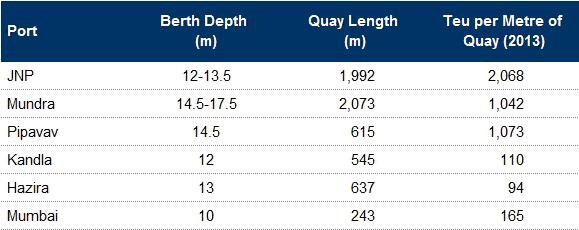

The private ports have managed to add capacity to meet market needs whilst JNP’s insufficient investment has seen its volumes hit a temporary ceiling due to high utilisation levels. In fact, due the pressure it is under, JNP operates at exceptionally intensive levels by world standards, achieving average throughput of over 2,000 teu per metre of quay per annum. The port’s continued importance is also despite its draft limitations of 12-13.5 metres compared with 14.5 metres as Pipavav and up to 17.5 metres at Mundra.

Figure 3 Upper West Coast and Greater Mumbai ports: Estimated Utilisation Levels, 2013

Source: Drewry Maritime Research

Source: Drewry Maritime Research

Table 1Maximum Berth Depth and Quayline Performance, UpperWest Coast and Greater Mumbai Ports

Source: Drewry Maritime Research

Source: Drewry Maritime Research

Terminal capacity and water depth are key factors in carriers’ network strategies. For example, most carriers currently operate separate Asia/West Coast India and Asia/Middle East services due to the delays and congestion at Indian ports, especially JNP. Enhanced capacity and water depth at JNP, complementing that at the likes of Mundra and Pipavav, would allow carriers to combine Asia – West Coast India and Asia – Middle East services in much the same way as they do for services from Europe to the Middle East and West Coast India.However, despite the improved environment for terminal investment in India, change at JNP is not just around the corner. Whilst the rapid development of new capacity by DP World will provide some respite, it is likely that the new PSA terminal will not become operational until at least 2017-18. Moreover, there are many rail and road bottlenecks to overcome. In addition, the progress of the JNP channel dredging project is also unclear.Across the bay, in Mumbai, the long delayed Mumbai offshore terminal project is still being pursued, although, once again, 2017-18 appears to be the very earliest that it is likely to become a reality. In the meantime Mundra and Pipavav appear to be in comfortable positions – but JNP will remain the lowest common denominator for carriers’ strategies when calling at the Indian West Coast.

Table 2Status of Capacity Expansion Plans, Upper West Coast and Greater Mumbai Ports

Source: Drewry Maritime Research

Source: Drewry Maritime Research

Our View

Reformed tariff legislation is already benefitting the Indian port sector by encouraging port capacity expansion in key container gateways like JNP. Carriers will soon be able to start rationalising services, therefore, but the pace of change will be slow.

Take away its congestion, and ocean carriers would no longer have to worry about vessels being delayed there before going on to other countries.In this respect, the port has seen two key events in the last few weeks – firstly the laying of the foundation stone for the expansion of capacity by 800,000 teu by DP World, with rapid completion targeted for 2015, and secondly the approval of PSA as winning bidder for the development of a huge new terminal at the port, with an ultimate capacity of 4.8 million teu p.a. – more than double the port’s present 4.1 million teu capacity. The PSA announcement is particularly noteworthy given that the company was previously part of a successful joint venture bid for this project before negotiations broke down amongst legal acrimony.Significant in this context is the recent decision by the Indian Government to partially relax the strict tariff regulation which applies to terminals in its designated major public ports. The PSA project will likely be the first to benefit from this.

The more relaxed rules will allow terminal operators to raise their tariffs every year based on market conditions (subject to a cap of 15%) provided agreed performance standards are met. This change should make investment in terminals in the major ports more viable and less risky, and help accelerate the addressing of congestion and capacity shortages. For a while it looked like existing terminals in the major ports would have to continue to live with the full tariff regulation as the change was not retrospective, but a recent move looks likely to ensure a level playing field.Private ports like Mundra and Pipavav, just up the coast, have always been outside the central Government tariff regulation scheme, and this is one factor that has allowed them to grow at the expense of the likes of JNP, along with having deeper water and available capacity. Volumes at Mundra for example increased by 28% in 2013 to over 2 million teu making it the country’s second largest container port. It has an estimated deep water capacity of 3.6 million teu p.a. and now includes a joint venture terminal with TIL (MSC).

Figure 1 Regional Split, Indian Container Port Traffic, 2013 (M teu)

Source: Drewry Maritime ResearchFigure 2 Upper West Coast and Greater Mumbai: Volumes by Port, 2013 (M teu)

Source: Drewry Maritime ResearchThe private ports have managed to add capacity to meet market needs whilst JNP’s insufficient investment has seen its volumes hit a temporary ceiling due to high utilisation levels. In fact, due the pressure it is under, JNP operates at exceptionally intensive levels by world standards, achieving average throughput of over 2,000 teu per metre of quay per annum. The port’s continued importance is also despite its draft limitations of 12-13.5 metres compared with 14.5 metres as Pipavav and up to 17.5 metres at Mundra.

Figure 3 Upper West Coast and Greater Mumbai ports: Estimated Utilisation Levels, 2013

Source: Drewry Maritime ResearchTable 1Maximum Berth Depth and Quayline Performance, UpperWest Coast and Greater Mumbai Ports

Source: Drewry Maritime ResearchTerminal capacity and water depth are key factors in carriers’ network strategies. For example, most carriers currently operate separate Asia/West Coast India and Asia/Middle East services due to the delays and congestion at Indian ports, especially JNP. Enhanced capacity and water depth at JNP, complementing that at the likes of Mundra and Pipavav, would allow carriers to combine Asia – West Coast India and Asia – Middle East services in much the same way as they do for services from Europe to the Middle East and West Coast India.However, despite the improved environment for terminal investment in India, change at JNP is not just around the corner. Whilst the rapid development of new capacity by DP World will provide some respite, it is likely that the new PSA terminal will not become operational until at least 2017-18. Moreover, there are many rail and road bottlenecks to overcome. In addition, the progress of the JNP channel dredging project is also unclear.Across the bay, in Mumbai, the long delayed Mumbai offshore terminal project is still being pursued, although, once again, 2017-18 appears to be the very earliest that it is likely to become a reality. In the meantime Mundra and Pipavav appear to be in comfortable positions – but JNP will remain the lowest common denominator for carriers’ strategies when calling at the Indian West Coast.

Table 2Status of Capacity Expansion Plans, Upper West Coast and Greater Mumbai Ports

Source: Drewry Maritime ResearchOur View

Reformed tariff legislation is already benefitting the Indian port sector by encouraging port capacity expansion in key container gateways like JNP. Carriers will soon be able to start rationalising services, therefore, but the pace of change will be slow.