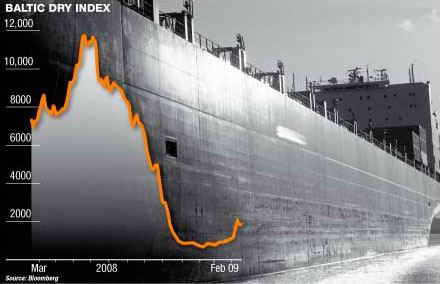

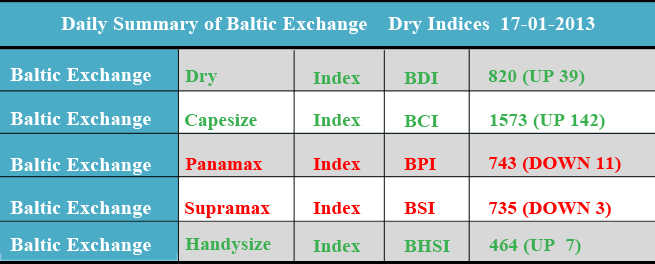

The dry bulk market has continued its climbing trend yesterday, as the industry's benchmark, the Baltic Dry Index (BDI) was up by 39 points to 820.The leading market was the Capesize one, with the BCI (Baltic Capesize Index) rising by 142 points to 1,573. Handysizes were also a bit higher, while the two other major subsegments retreated by 11 (Panamaxes) and 3 points (Supramaxes) respectively. According to the latest weekly report from shipbroker Fearnleys, commenting on the Capesize segment it noted that "signals are mixed but the overall tendency is positive, with Atlantic leading the way. The Tubarao/Qingdao conference trade is showing strength, with major takers out to book tonnage for February dates at "last done or touch better" - next fixture expected to be USD 19 pmt or close, up some USD 1. 50 pmt or around USD 15% in net earnings w-o-w. Pacific levels follow suit, although volume in this area is limited. Paper is giving renewed support for period activity, and notable fixture include 176k dwt/built 2012 done for 8/12 months at USD 10250 basis China end January, 180k dwt/built 2011 for 8/12 months at USD 10750 basis China prompt, and an even stronger 161k dwt/built 1996 for 8/12 months at USD 10k basis China prompt" it noted.In a similar note, Shiptrade & Services had noted on the Capesize market that it was a positive week, with rates increasing steadily. "The Atlantic market has shown a relatively positive week with the Tubarao/Qingdao route yielding TCE of about USD 17,250 improved by 500 USD and the transantlantic round trips closing at around USD 6,750/USD 7,000 increased by USD 1,250 compared to last week’s levels.  As for the fronthaul trade, fixture has been concluded ex EMed via Bsea to China at USD 26,000. Despite the cyclone which hit West Australia and affected negatively iron ore trade, Pacific market slightly picked up with the round trips ending up at around USD 6,750 improved by USD 750. Period levels at around USD 10,250 for one year" the shipbroker said.

On the Panamax front, Fearnleys added that "after a positive drive last week, driven by fresh Atlantic cargoes and ECSA loaders, the market has come to a halt with a decline in both volumes and levels. Both the Atlantic and the Pacific is definitely slower, with still a few but not enough fresh cargo injection and seem at best to be consolidating before any new clear direction is proven. Still large amount of newbuidings are coming out of yards and number of ballasting dir RBCT/ECSA is increasing. Atlantic rounds are pending between 6k for short rounds and 8k for 2ll. Fronthaul paying like 14k with a premium for Baltic loading. Whilst in the Pacific owners ask 7k DOP for ECSA rounds with less takers, the Indo/India rounds have come down to 5 + 50 APS. The period market is drying up after a few longer deals done end of last/early this week including a super eco Kamsarmax at 9k for 18-24 months. Owners now ask 7k+ for short period, but takers are focused on new eco design and wide spreads to consider same" the shipbroker concluded.

Finally, in the Handysize front, it noted that "the Atlantic market remained stable with USG-Feast fixed around USD 17k. Continent/Mediterranean-Feast fixed at USD 10k. The Pacific market remained weak with lot of ships and less cargoes. Indo-India round now fixed at APS 8k + BB 120k. Nopac round fixed at APS 7500 + BB 300k. RBCT round fixed at APS USD 8500 + BB 300k. Red Sea fertilizer cargo to India fixed at mid teens. Short period activity was limited and rates around USD 8500 for large eco Supra" Fearnleys said. On the Supramax front in particular, Shiptrade added that "there was finally some optimism in the Atlantic Basin as fresh cargoes emerged this week giving positive trend on the USG and ECSA area.Even though there is lack of prompt tonnage especially in the USG, charterers with firm requirements in their hands will cover them quickly supporting the positive trend. As from ECSA, trips to FEast are paying around USD 12-13k + 2-300k BB depending on size. Transatlantic trips were more neutral on prompt dates. Rates seen are around Mid - High teens depending on the redelivery. Trips from the Emed to USG are expected to pay around USD 2,500 whereas direction Continent the rates hover around USD 5,000 depending on the redelivery. Scrap cargoes to EMed fluctuate at levels close to USD 8,000, whereas trips FEast are getting fixed at low teens. The Pacific Market finally reacted but only to settle back again after the middle of the week. Indo round voyage rates above USD 10,000 delivery Singapore to China, whereas for trips delivery ECI via Indo to India pay around USD 8,000 depending on the redelivery. NOPAC rounds are not very active but some requirements were seen and ratewise around USD 7,000 + 350/400k BB should be expected. Some interest from charterers has been observed for short period and rates are around USD 8,000 – 9,000 depending on size and delivery point" the shipbroker concluded.

As for the fronthaul trade, fixture has been concluded ex EMed via Bsea to China at USD 26,000. Despite the cyclone which hit West Australia and affected negatively iron ore trade, Pacific market slightly picked up with the round trips ending up at around USD 6,750 improved by USD 750. Period levels at around USD 10,250 for one year" the shipbroker said.

On the Panamax front, Fearnleys added that "after a positive drive last week, driven by fresh Atlantic cargoes and ECSA loaders, the market has come to a halt with a decline in both volumes and levels. Both the Atlantic and the Pacific is definitely slower, with still a few but not enough fresh cargo injection and seem at best to be consolidating before any new clear direction is proven. Still large amount of newbuidings are coming out of yards and number of ballasting dir RBCT/ECSA is increasing. Atlantic rounds are pending between 6k for short rounds and 8k for 2ll. Fronthaul paying like 14k with a premium for Baltic loading. Whilst in the Pacific owners ask 7k DOP for ECSA rounds with less takers, the Indo/India rounds have come down to 5 + 50 APS. The period market is drying up after a few longer deals done end of last/early this week including a super eco Kamsarmax at 9k for 18-24 months. Owners now ask 7k+ for short period, but takers are focused on new eco design and wide spreads to consider same" the shipbroker concluded.

Finally, in the Handysize front, it noted that "the Atlantic market remained stable with USG-Feast fixed around USD 17k. Continent/Mediterranean-Feast fixed at USD 10k. The Pacific market remained weak with lot of ships and less cargoes. Indo-India round now fixed at APS 8k + BB 120k. Nopac round fixed at APS 7500 + BB 300k. RBCT round fixed at APS USD 8500 + BB 300k. Red Sea fertilizer cargo to India fixed at mid teens. Short period activity was limited and rates around USD 8500 for large eco Supra" Fearnleys said. On the Supramax front in particular, Shiptrade added that "there was finally some optimism in the Atlantic Basin as fresh cargoes emerged this week giving positive trend on the USG and ECSA area.Even though there is lack of prompt tonnage especially in the USG, charterers with firm requirements in their hands will cover them quickly supporting the positive trend. As from ECSA, trips to FEast are paying around USD 12-13k + 2-300k BB depending on size. Transatlantic trips were more neutral on prompt dates. Rates seen are around Mid - High teens depending on the redelivery. Trips from the Emed to USG are expected to pay around USD 2,500 whereas direction Continent the rates hover around USD 5,000 depending on the redelivery. Scrap cargoes to EMed fluctuate at levels close to USD 8,000, whereas trips FEast are getting fixed at low teens. The Pacific Market finally reacted but only to settle back again after the middle of the week. Indo round voyage rates above USD 10,000 delivery Singapore to China, whereas for trips delivery ECI via Indo to India pay around USD 8,000 depending on the redelivery. NOPAC rounds are not very active but some requirements were seen and ratewise around USD 7,000 + 350/400k BB should be expected. Some interest from charterers has been observed for short period and rates are around USD 8,000 – 9,000 depending on size and delivery point" the shipbroker concluded.

As for the fronthaul trade, fixture has been concluded ex EMed via Bsea to China at USD 26,000. Despite the cyclone which hit West Australia and affected negatively iron ore trade, Pacific market slightly picked up with the round trips ending up at around USD 6,750 improved by USD 750. Period levels at around USD 10,250 for one year" the shipbroker said.

On the Panamax front, Fearnleys added that "after a positive drive last week, driven by fresh Atlantic cargoes and ECSA loaders, the market has come to a halt with a decline in both volumes and levels. Both the Atlantic and the Pacific is definitely slower, with still a few but not enough fresh cargo injection and seem at best to be consolidating before any new clear direction is proven. Still large amount of newbuidings are coming out of yards and number of ballasting dir RBCT/ECSA is increasing. Atlantic rounds are pending between 6k for short rounds and 8k for 2ll. Fronthaul paying like 14k with a premium for Baltic loading. Whilst in the Pacific owners ask 7k DOP for ECSA rounds with less takers, the Indo/India rounds have come down to 5 + 50 APS. The period market is drying up after a few longer deals done end of last/early this week including a super eco Kamsarmax at 9k for 18-24 months. Owners now ask 7k+ for short period, but takers are focused on new eco design and wide spreads to consider same" the shipbroker concluded.

Finally, in the Handysize front, it noted that "the Atlantic market remained stable with USG-Feast fixed around USD 17k. Continent/Mediterranean-Feast fixed at USD 10k. The Pacific market remained weak with lot of ships and less cargoes. Indo-India round now fixed at APS 8k + BB 120k. Nopac round fixed at APS 7500 + BB 300k. RBCT round fixed at APS USD 8500 + BB 300k. Red Sea fertilizer cargo to India fixed at mid teens. Short period activity was limited and rates around USD 8500 for large eco Supra" Fearnleys said. On the Supramax front in particular, Shiptrade added that "there was finally some optimism in the Atlantic Basin as fresh cargoes emerged this week giving positive trend on the USG and ECSA area.Even though there is lack of prompt tonnage especially in the USG, charterers with firm requirements in their hands will cover them quickly supporting the positive trend. As from ECSA, trips to FEast are paying around USD 12-13k + 2-300k BB depending on size. Transatlantic trips were more neutral on prompt dates. Rates seen are around Mid - High teens depending on the redelivery. Trips from the Emed to USG are expected to pay around USD 2,500 whereas direction Continent the rates hover around USD 5,000 depending on the redelivery. Scrap cargoes to EMed fluctuate at levels close to USD 8,000, whereas trips FEast are getting fixed at low teens. The Pacific Market finally reacted but only to settle back again after the middle of the week. Indo round voyage rates above USD 10,000 delivery Singapore to China, whereas for trips delivery ECI via Indo to India pay around USD 8,000 depending on the redelivery. NOPAC rounds are not very active but some requirements were seen and ratewise around USD 7,000 + 350/400k BB should be expected. Some interest from charterers has been observed for short period and rates are around USD 8,000 – 9,000 depending on size and delivery point" the shipbroker concluded.