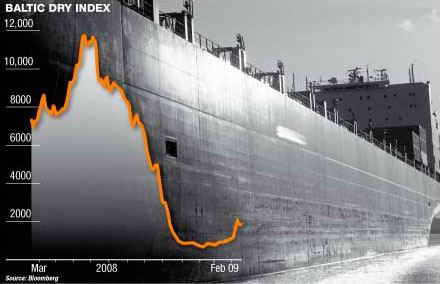

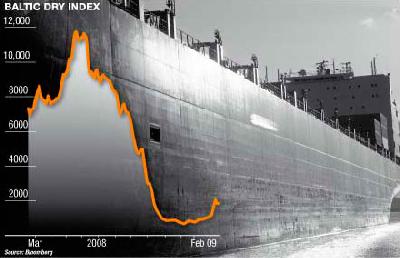

The dry bulk market has finally halted its plunge, after a devastating week of yet more losses. The industry’s benchmark, the Baltic Dry Index (BDI) has stayed lull at 1,439 points the lowest it’s been since April of 2009 and October of 2008. Still, yesterday, the capesize index lost an additional 0.31%, while the Panamax segment fell by 1.87 percent. The only “survivor” of the market was the smalle handysize segment which yesterday gained 1.05%.

The dry bulk market has finally halted its plunge, after a devastating week of yet more losses. The industry’s benchmark, the Baltic Dry Index (BDI) has stayed lull at 1,439 points the lowest it’s been since April of 2009 and October of 2008. Still, yesterday, the capesize index lost an additional 0.31%, while the Panamax segment fell by 1.87 percent. The only “survivor” of the market was the smalle handysize segment which yesterday gained 1.05%.According to Paris-based shipbroker Barry Rogliano Salles (BRS), dry bulk rates kept falling, mainly as a result of weather-related problems affecting the short-term outlook, and newbuilding deliveries the longer-term picture.

“Rising commodity prices indicate there is still good demand for product, which suggests newbuilding deliveries are the main issue affecting rates. After two weeks of 2011, 20 new Capes have been delivered, 9 Panamaxes, 28 Supramaxes, and 21 Handysizes, indicating the pace of delivery is increasing. In the FFA market, 2H 2011 is now trading at around US$21,000 per day compared to US$24,000 six months ago” said the shipbroker. Regarding the beleaguered Capesize market, it’s been another period of softening rates, with the BCI losing an additional 15% last week, with the Cape 4TC, at just under $9,700, being now below the time charter equivalent for all the other bulk sizes. “Players reported a sharp drop in Australian business, with coal operations still disrupted due to weather factors, and a lacklustre demand for ore. In the period market, it was reported that a 161,000 tonner was taken for 3-5 months at US$13,000 per day. However the sole one-year charter was signed at a BCI index-linked rate. On Monday however the BCI lost just 5 points, raising hopes among owners that the market may be bottoming out” said the report.

All this freight rate saga has altered things in the second hand sale and purchase market. According to BRS “the recent fall in freight rates has created a gap between Buyers and Sellers when it comes to prices, resulting in a very quiet S&P market. We expect this to last for the next few weeks until maybe after the Chinese New Year. This week's S&P menu is all about ‘age’, as in ‘overaged’, and ‘old age’ etc. Arcelor Mittal have sold their Panamax ‘Kirti’ (68,000 dwt, built 1986 in Japan) to Chinese buyers for about US$10m. We understand that this is a December 2010 sale and that the vessel is due for SS & DD in April 2011, just after delivery to the buyers.

Excel Maritime of Greece have sold their Handymax ‘Marybelle’ (43,000 dwt, built 1987 in Japan) to Bangladeshi buyers for a price in the region of US$10.8m, which also seems to be a December 2010 sale. In probably the most active week involving Egyptian interests we note that the National Navigation Co of Egypt have sold their sister Handies ‘Alwadi Al Gadeed’ and ‘Wadi Halfa’ (32,000 dwt, built 1985 in South Korea) for about US$7m each. At the same time Egyptian buyers have reportedly agreed a price in the region of US$6m for the Greek owned ‘Androniki’ (30,000 dwt, built 1984 in Japan) - yielding a nice return for the Seller who purchased the ship back in March 2009 as the ‘Manora Naree’ for US$2.9m from Precious in Thailand” concluded BRS.

In total, Piraeus-based shipbroker Golden Destiny reported 35 sales (including demolition activity) during the course of the previous week. “In the secondhand market, 27 vessels were reported to have changed hands this week equalling a total amount of money invested in the region of US$ 1,3 million, with 6 transactions reported for an undisclosed price. In terms of reported number of transactions, the S&P activity has been marked with a 28.5% positive w-o-w change and a 31% negative change comparable with previous year’s weekly S&P activity. The tanker sector attracted most attention, with an investment capital of $ 658,744 around 50% share of the total invested capital in the S&P secondhand market.

In the demolition market, 8 vessels reported to have been headed to the scrap yards of total deadweight just 310,651, with India attracting most activity. Despite the attractive price levels above 450 $/ldt and even surpassing the 500 $/ldt barrier, the reported transactions in terms of number of vessels heading the scrap yards remains at similar levels of last week. The Greek (but not greek based) presence has been noticed this week in 4 transactions reported in the secondhand and one in the newbuilding market. The preference in the secondhand market was towards the chemical tanker sector and a passenger vessel of 1585 passenger capacity, while the total invested capital was region $ 43 mil. In the newbuilding market the greek presence was noticed in the panamax bulkcarrier sector, with Safe Bulkers announcing to have contracted the subject vessel at region $ 41.7 mil” said Golden Destiny.