In 2013, global seaborne coking coal trade grew firmly, and is estimated to have expanded 13% y-o-y to 266mt, following a 5% contraction in 2011 and a 6% recovery in 2012.

China’s coking coal import growth in 2013 is estimated to have accounted for around 80% of global coking coal trade growth in 2013. Two factors have been key in driving this growth. Chinese imports in 2013 are estimated to have grown rapidly by 71% y-o-y to total 59mt. A major driver of this growth was relatively low international coking coal prices.

China has vast domestic reserves of coking coal and so import volumes are largely affected by the price differential between international coking coal and domestic (Chinese) coking coal.In early 2011, floods in Australia significantly restricted coking coal supply.

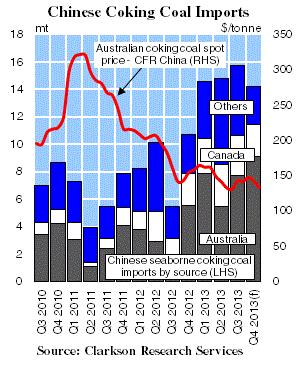

The Graph of the Month shows that the Australian coking coal spot price exceeded $300/tonne in 2011 and China’s imports fell 46% q-o-q from 7.3mt in Q1 to 4.0mt in Q2 2011. Since May 2011, international coking coal prices have fallen as Aus-tralian supply has recovered, helping prices to average $146/tonne in 2013, down 19% from $181/tonne in 2012.Disruptive DriversChinese seaborne imports in 2013 were also affected by limited landborne supply. In the first eleven months of 2013, landborne Mongolian coking coal exports to China fell 21% y-o-y to 13mt as financial difficulties associated with the country’s largest coking coal mine restricted supply.

This further supported demand for seaborne imports, with monthly volumes peaking at 5.7mt in January 2013. Despite a slight recovery in Mongolian supply in the latter part of 2013, Chinese imports from Australia remained at high levels of around 2.5mt/month.Australian InfluenceThis was partly due to the greater availability of Australian coking coal as output rose firmly last year following disruptions from flooding and strikes in 2011-12. As a result, Australian growth accounted for a significant proportion (74%) of the increase in Chinese seaborne imports in 2013.

Chinese imports from Australia in the first eleven months of 2013 totalled 26.8mt, compared to 11.0mt in the same period of 2012 which represents y-o-y growth of 144%. This drove an increase in the share of Chinese seaborne coking coal imports sourced from Australia from 40% in 2012 to 50% in 2013. However, the volume of coking coal imports from other suppliers also rose, with Chinese imports from Canada in 2013 more than three times that in 2011.Since coking coal prices have a major impact on Chinese and global trade, prospects for 2014 remain heavily dependent on Australian supply trends. Providing there are no greater than usual disruptions to supply in Q1, Australia’s exports are expected to grow by 6% and Chinese imports are projected to increase by 11% in 2014. While growth is unlikely to be as rapid as in 2013, China is expected to provide at least half of the growth in global coking coal trade in 2014.

China’s coking coal import growth in 2013 is estimated to have accounted for around 80% of global coking coal trade growth in 2013. Two factors have been key in driving this growth. Chinese imports in 2013 are estimated to have grown rapidly by 71% y-o-y to total 59mt. A major driver of this growth was relatively low international coking coal prices.

China has vast domestic reserves of coking coal and so import volumes are largely affected by the price differential between international coking coal and domestic (Chinese) coking coal.In early 2011, floods in Australia significantly restricted coking coal supply.

The Graph of the Month shows that the Australian coking coal spot price exceeded $300/tonne in 2011 and China’s imports fell 46% q-o-q from 7.3mt in Q1 to 4.0mt in Q2 2011. Since May 2011, international coking coal prices have fallen as Aus-tralian supply has recovered, helping prices to average $146/tonne in 2013, down 19% from $181/tonne in 2012.Disruptive DriversChinese seaborne imports in 2013 were also affected by limited landborne supply. In the first eleven months of 2013, landborne Mongolian coking coal exports to China fell 21% y-o-y to 13mt as financial difficulties associated with the country’s largest coking coal mine restricted supply.

This further supported demand for seaborne imports, with monthly volumes peaking at 5.7mt in January 2013. Despite a slight recovery in Mongolian supply in the latter part of 2013, Chinese imports from Australia remained at high levels of around 2.5mt/month.Australian InfluenceThis was partly due to the greater availability of Australian coking coal as output rose firmly last year following disruptions from flooding and strikes in 2011-12. As a result, Australian growth accounted for a significant proportion (74%) of the increase in Chinese seaborne imports in 2013.

Chinese imports from Australia in the first eleven months of 2013 totalled 26.8mt, compared to 11.0mt in the same period of 2012 which represents y-o-y growth of 144%. This drove an increase in the share of Chinese seaborne coking coal imports sourced from Australia from 40% in 2012 to 50% in 2013. However, the volume of coking coal imports from other suppliers also rose, with Chinese imports from Canada in 2013 more than three times that in 2011.Since coking coal prices have a major impact on Chinese and global trade, prospects for 2014 remain heavily dependent on Australian supply trends. Providing there are no greater than usual disruptions to supply in Q1, Australia’s exports are expected to grow by 6% and Chinese imports are projected to increase by 11% in 2014. While growth is unlikely to be as rapid as in 2013, China is expected to provide at least half of the growth in global coking coal trade in 2014.