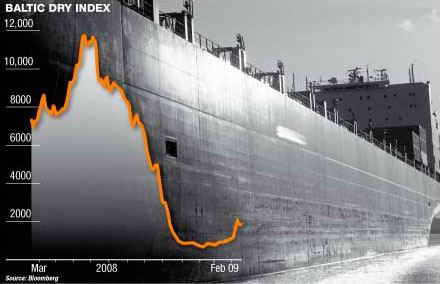

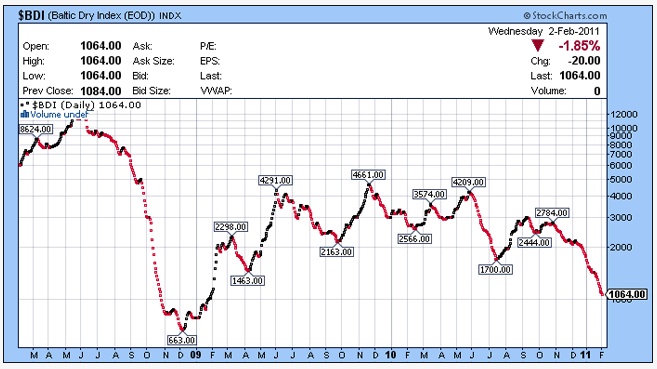

With the dry bulk market having lost more than 72% of its value in the last month or so and having retreated to a 2-year low, it seems that the bottom has almost been reached. The combination of devastating floods in Queensland, the richest coal producing province of Australia and in fact globally and the looming closure of China’s factories for the celebration of the new Lunar Year,have contributed to the dry bulk industry’s benchmark, the Baltic Dry Index (BDI) now being at 1,064 points, losing 1.64% after yesterday’s session. Once again, it was the Supramaxes that suffered the most, losing 2.35%.

But a new report out yesterday from JP Morgan could be seen as a cheerful note, since it suggested that the catastrophic dry bulk market is now bottoming out. “We believe that freight rates are bottoming out,” JP Morgan shipping analysts wrote, predicting a rash of scrapping for ships aged 20-years-old or more. Moreover, JP Morgan analysts stressed they felt the recent collapse in the Baltic Dry Index, that sees capesizes trading for less than $7,000 a day, was more weather-related than structural. JP Morgan cited China Cosco as a buy, noting it was “the most leveraged BDI play for investors with higher risk appetite”. Pacific Basin was also cited “for investors who are more risk averse as it has covered c.50% of its revenue days this year and net cash”. MOL, U-Ming and Sincere were all deemed worth investing in too.

In its latest weekly report, shipbroker Fearnley’s said for the capesize market, that it was “another quiet week, with political disturbances affecting the oil prices. Vessels, in ballast, towards South Africa/Brazil who have already bunkered in Singapore have a competitive advantage over vessels just starting to ballast. Higher bunker prices are being reflected in present rates offered, but so far, owners have been unable to conclude on this basis. It seems as though this current price increase will be borne by the owner. With market levels below operating costs, cyclones again hitting Australia and Chinese New Year, the immediate future look bleak, with more and more owners willing to wait rather than fixing in the current climate. One period fixture has been concluded at below usd 20k per day but with delivery in the Atlantic and a profit sharing scheme” said Fearnley’s.

As for the smaller Handysize/Handymax segment which has been battered this week, it said that it is an extremely quiet market in the Atlantic, “with a lot of spot tonnage struggling to get covered. Charterers are shying away from fixing short period as they expect further misery ahead. Rates for t/a rounds in the very low teens as USG markets are the only relatively paying areas. Nevertheless the high amount of ballasting tonnage towards USG will most certainly exerce further stronger downward pressure on rates. The Continent is not active at all. Outlook: Grim. Activity remains quiet in the F.East and seems no relief for owners. Supras getting under usd 5000 bss North China dely for Indo-India and Thailand rounds. From WCI, rates remained steady around usd 15-16k and from ECI USD 12k for trip to east. Some believe Indian iron ore activity to pick up after Chinese holidays. RBCT rounds around usd 13k bss WCI. Short period rates for Supras still around USD 14k. Handymax cargoes from Red Sea to India are fixed around low-mid 20s on voyage” it said.

Regarding the Panamax market, the report mentioned that as Chinese New Year holidays began yesterday, “the activity level slowed down even further. With a cyclone approaching Australia and an already over-supply of tonnage in the Pacific, several Panamaxes were ballasting towards the USG. Approximately 60 vessels were reported sailing inbound this week. This of course put more pressure on the Atlantic basin which already struggled with its tonnage/cargo ratio. Pacific rounds fixed usd 7500 and TA´s usd 10500, fronthauls USD 19600 and backhauls USD 3400. The period market has almost vanished the last couple of weeks. Even so, some short period deals have been reported done in the region 15-15,5k” it concluded.