In the 2000s new ships were the in thing. Public companies boasted about their youthful fleets and since ships were floating cash machines, who could argue? Why buy old ships that might break down during a boom, costing cash instead of coining it? But today youth weighs heavily on balance sheets and suddenly older ships look interesting.

Good and Old:

But should they? With a surplus of tankers and bulkcarriers it would suit many investors if the old ships quietly left the market. That's what happens in recessions - the new technology chases out the over-age and obsolete ships, leaving a more efficient and eco-friendly fleet to lead the industry into the upswing. But, convenient though this would be for owners of new tonnage, realizing this scenario in today's market faces two obstacles.

Not So Obsolete, Actually

The first is that ship technology has not changed much in the last 20 years, so well maintained old ships do not carry a big cost penalty, especially when slow steaming. On paper the new generation eco-ships might knock 10% off consumption, but many of the improvements can be retrofitted. The market seems to agree, bidding the price of a 10-year-old Panamax bulker up by 52% since the end of September 2013.

The first is that ship technology has not changed much in the last 20 years, so well maintained old ships do not carry a big cost penalty, especially when slow steaming. On paper the new generation eco-ships might knock 10% off consumption, but many of the improvements can be retrofitted. The market seems to agree, bidding the price of a 10-year-old Panamax bulker up by 52% since the end of September 2013.

Meanwhile new ships face eye-watering capital costs. Although interest is low, bank lending margins are high and interest rates will probably rise. Also new ships face heavy depreciation. For example at today's prices, depreciating a new VLCC, might cost $13,000 per day. Admittedly it's not cash, but ignoring depreciation is a dangerous game.

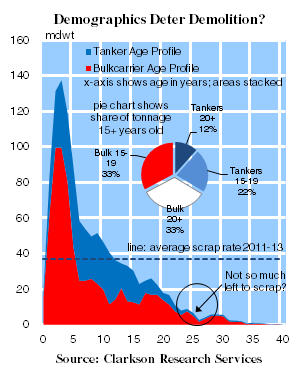

Not Much to Scrap About

The second obstacle to ditching the old ships is that in these sectors there are not so many of them left. The normal scrapping age for merchant ships is 20-30 years, which today means ships built 1984-94. In those days there were few deliveries, and the age profile of the bulk fleet is very skewed. Only 79m dwt of bulkers and 28m dwt of tankers are 20 years old or above. At recent scrapping volumes that's about three years of demolition. There's another 127m dwt of 15-19 year old tonnage, but would investors pay $14.5m for a 15 year old Panamax if they thought it was a possible scrap candidate?

New Ships or Old?

So there you have it. The shipping market is in the trough and investors’ eyes are on the future. Shipyards have made headlines, recording orders for 158.2m dwt of new ships in 2013, almost 3 times as much as in 2012. With a sizeable overhang of surplus tonnage, the market is going to need all the help it can get to squeeze rates to a level which will provide some sort of profit for investors. In the last 3 years scrapping has helped by removing 37m dwt of tankers and bulkers a year. But the really old ships are now thin on the ground and the younger generation don't look very obsolete. So don't rely too much on scrapping to solve the surplus problem. Have a nice day.

Good and Old:

But should they? With a surplus of tankers and bulkcarriers it would suit many investors if the old ships quietly left the market. That's what happens in recessions - the new technology chases out the over-age and obsolete ships, leaving a more efficient and eco-friendly fleet to lead the industry into the upswing. But, convenient though this would be for owners of new tonnage, realizing this scenario in today's market faces two obstacles.

Not So Obsolete, Actually

The first is that ship technology has not changed much in the last 20 years, so well maintained old ships do not carry a big cost penalty, especially when slow steaming. On paper the new generation eco-ships might knock 10% off consumption, but many of the improvements can be retrofitted. The market seems to agree, bidding the price of a 10-year-old Panamax bulker up by 52% since the end of September 2013.Meanwhile new ships face eye-watering capital costs. Although interest is low, bank lending margins are high and interest rates will probably rise. Also new ships face heavy depreciation. For example at today's prices, depreciating a new VLCC, might cost $13,000 per day. Admittedly it's not cash, but ignoring depreciation is a dangerous game.

Not Much to Scrap About

The second obstacle to ditching the old ships is that in these sectors there are not so many of them left. The normal scrapping age for merchant ships is 20-30 years, which today means ships built 1984-94. In those days there were few deliveries, and the age profile of the bulk fleet is very skewed. Only 79m dwt of bulkers and 28m dwt of tankers are 20 years old or above. At recent scrapping volumes that's about three years of demolition. There's another 127m dwt of 15-19 year old tonnage, but would investors pay $14.5m for a 15 year old Panamax if they thought it was a possible scrap candidate?

New Ships or Old?

So there you have it. The shipping market is in the trough and investors’ eyes are on the future. Shipyards have made headlines, recording orders for 158.2m dwt of new ships in 2013, almost 3 times as much as in 2012. With a sizeable overhang of surplus tonnage, the market is going to need all the help it can get to squeeze rates to a level which will provide some sort of profit for investors. In the last 3 years scrapping has helped by removing 37m dwt of tankers and bulkers a year. But the really old ships are now thin on the ground and the younger generation don't look very obsolete. So don't rely too much on scrapping to solve the surplus problem. Have a nice day.